I hold a BSc in Banking and Finance. Here, on Seeking Alpha, I cover a variety of growth stocks and income stocks, including identifying those with the highest expected return potential, and a solid margin of safety.

Currently contributing as Promoting Author to the "Wheel of Fortune" marketplace.

Feel free to contact me at any time, and follow me here on S.A. for regular content and updates!

Happy investing!

Nick

Summary

While poised to grow significantly over the next couple of years, the Industrials sector features high valuations, which have priced in much of that growth already.

One of the stocks in the sector and amongst our holdings, Teekay LNG Partners L.P., has stood out, offering a superior investment case.

The stock's short-term upside is strong amid a potential valuation expansion, while its dividend yield is substantial and very well-covered.

Hence, the stock is our top Industrials pick for the rest of 2021.

Looking for a portfolio of ideas like this one? Members of Wheel of Fortune get exclusive access to our model portfolio. Learn More »

Photo by gremlin/E+ via Getty Images

On to the Industrials...

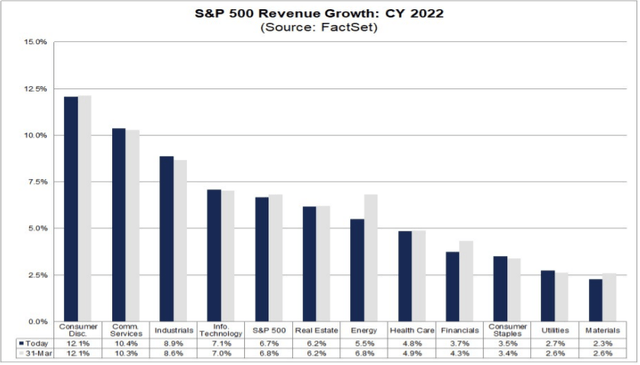

As we continue our anniversary series by covering each sector and its current state in the market, my co-Pilot on Wheel of Fortune, The Fortune Teller, has already published an article focusing on industrials. In that article, we go on to discuss why the current "house of cards" economy (which is built on money printing and endless debt), while arguably reckless, is set to boost the revenue growth of some sectors, with Industrials featuring one of the highest expected profitability growths over the next couple of years.

Source: FactSet

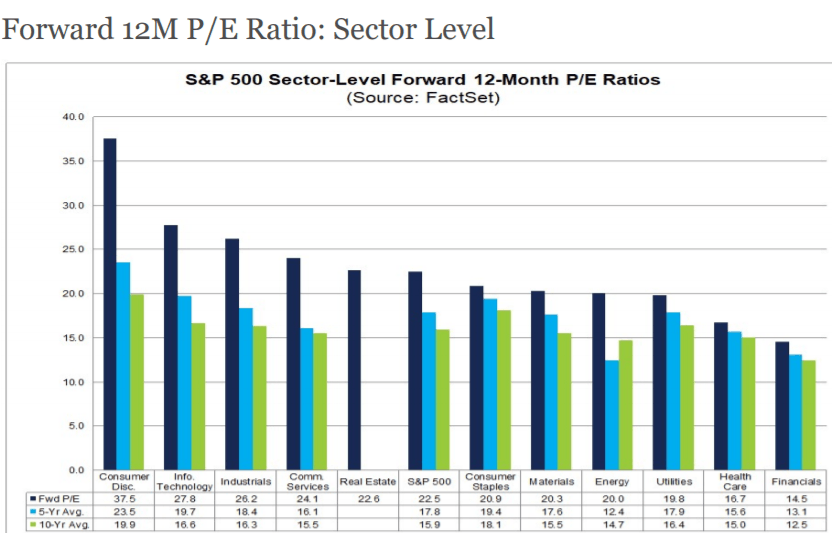

That being said, there is a bit of an issue. Frankly, much of that expected affluence seems to be already priced in, with industrials currently the third most expensive sector when measured on a forward 12-month P/E basis.

Source: FactSet

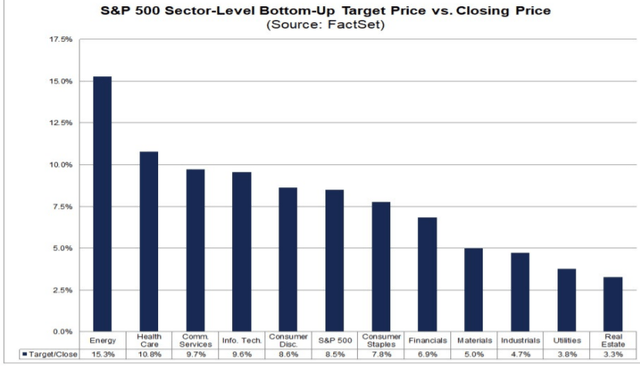

As a result, it doesn't come as a surprise that the Industrial sector is the third-worst one when it comes to the additional upside from current valuations. At 4.7%, only Utilities (3.8%) and Real Estate (3.3%) offer a lower price appreciation potential.

Source: FactSet

Therefore, when it came to picking attractively priced stocks in the sector, we had to dive into its sub-categories. Amongst them, we found the shipping industry to be currently offering the most fairly priced equities, despite enjoying a great rally since last year's March.

This article reveals our top pick in the sector for the rest of 2021, which amongst the various appealing stocks in the shipping industry, we believe it holds the highest short-term upside. That is, the Bermuda-based Teekay LNG Partners L.P. (NYSE:TGP), whose underlying financials and capital return potential are not reflected in the stock's current valuation, in our view.

Why Teekay LNG Partners

Firstly, it's important to note why TGP is an industry leader, displaying some incredibly high-quality characteristics.

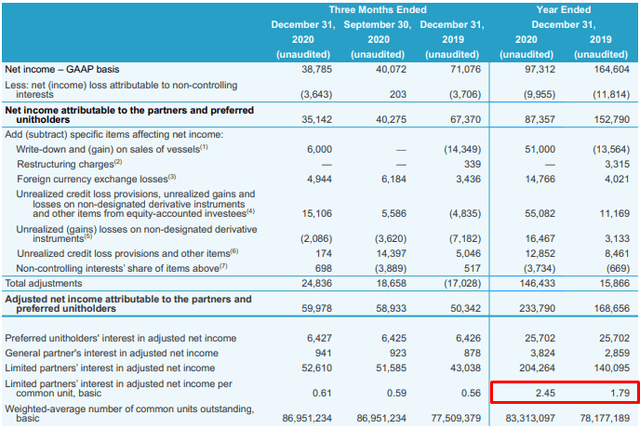

Despite the challenges caused by the ongoing pandemic during 2020, TGP's adjusted net income for the year came in at $234M, while its total adjusted EBITDA reached $758M, both of which were the best in the company's 16-year history.

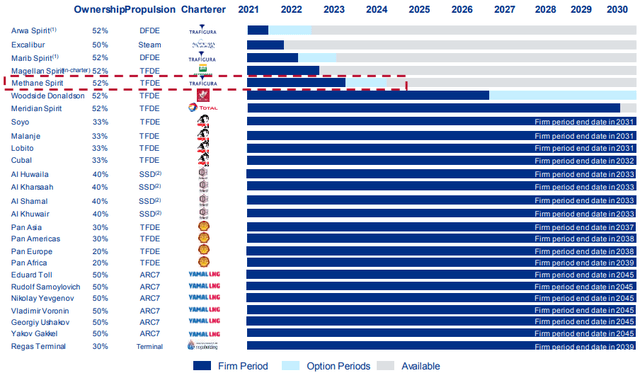

The reason TGP is able to post such resilient numbers lies in its ability to lock in multi-year charters that ensure predictable cash flows. This is due to the company's fleet being a critical infrastructure component to the LNG value chain. Following the two-plus year contract of its Methane Spirit near the end of Q4, the fixed contract percentage of TGP's LNG fleet currently stands at 97% and nearly 89% for 2021 and 2022, respectively.

With such a robust short-term cash flow security, as well as an average remaining contract tenor of 10+ years in TGP charters, we can safely say that the company is highly unlikely to experience wild fluctuations in its short- to medium-term financials. This has been the case in the past as well, with the company delivering resilient results, despite any volatile periods in the LNG industry.

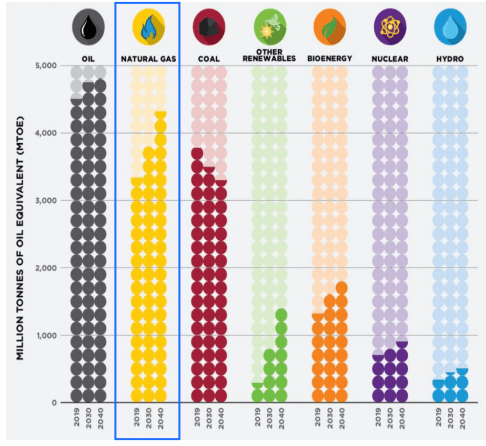

Additionally, with South and East Asia projected to drive additional demand for natural gas, which is expected to increase by 30% by 2040, the company is looking at a very favorable environment ahead to capitalize on, inspiring confidence in regards to its long-term operations as well. Keep in mind that TGP's fleet currently transports approximately 8% of the world's seaborne gas. Its market-leading position and cash flow security make for a great combo when it comes to capturing the gradually increasing demand for LNG going forward.

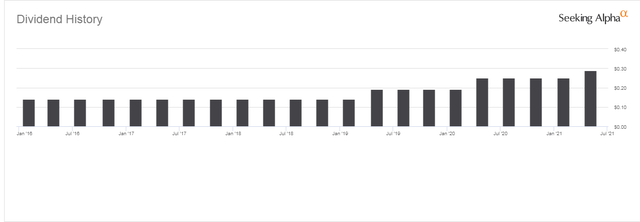

All this is great, but it would mean little if investors didn't get to enjoy TGP's success in their own regard, which translates to increased capital returns. Since 2016, the company has announced three double-digit distribution increases, with the most recent one hiking the quarterly rate by 15% to $0.2875, suggesting a 7.86% yield at TGP's current price levels.

Source: Seeking Alpha

Remember that while the shipping industry had a fantastic 2020, few companies currently offer meaningful capital returns to their shareholders. Other than Höegh LNG Partners LP (NYSE:HMLP) and KNOT Offshore Partners LP (NYSE:KNOP), whose yields are both hovering in the double digits, there are not any other common stocks/units offering such a high yield in the industry.

Despite the double-digit dividend increase, TGP's distributions should remain very well covered. With all liabilities such as interest expenses and preferred distribution already accounted for, TGP delivered adjusted EPS of $2.45 during 2020, very comfortably covering the $1.15 annualized distribution rate post the increase while retaining enough cash to continue paying down its debt.

Such a high yield which at the same time is amply covered should quickly signal a very inexpensive valuation, which is indeed the case with TGP.

There have been a couple of stocks that we are (or were) holding for a few years, but the majority of our shipping exposure was created during (or after) the "March Madness" of 2020. For simplicity, we bundle all these names, and we treat them as if they are lawful representatives of our shipping section to help us identify our top pick amongst them.

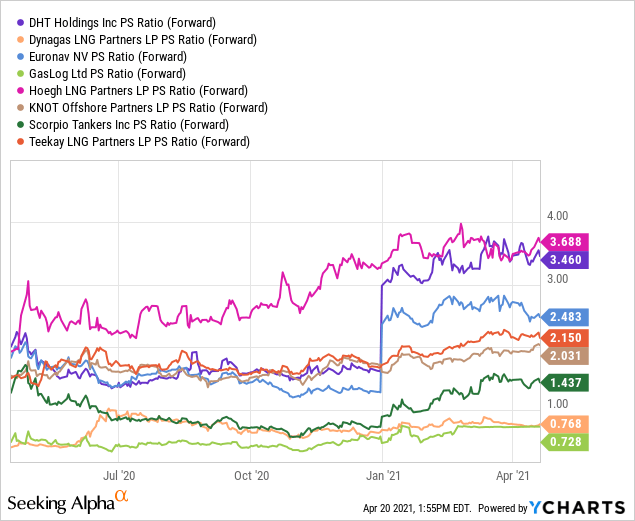

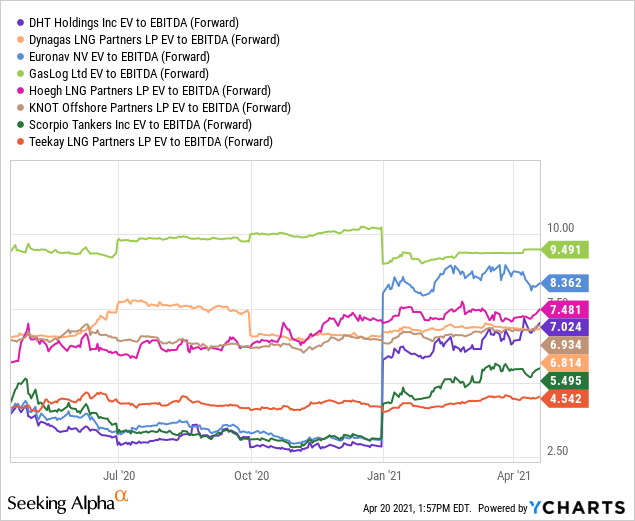

Let's take a look at these graphs below:

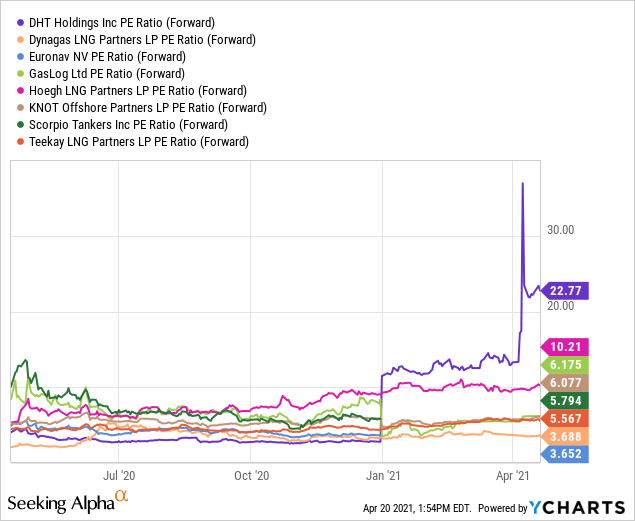

Forward P/E Ratio:

Forward P/S Ratio:

Forward EV/EBITDA Ratio:

Besides the valuations of these shipping names surely looking way better than the valuations of the Industrials sector as a whole, TGP seems to then have the best relationship between its valuation, risk, and reward.

At a forward EV/EBITDA of 4.5, TGP offers both a safe, sky-high yield and the potential for a substantial valuation expansion, which could result in hefty short-term gains (hence our top pick for 2021).

Companies such as HMLP and KNOP, as mentioned earlier, offer double-digit yields but little (to no) potential for additional capital gains upside. At the same time, companies like Scorpio Tankers (STNG) and DHT Holdings (DHT), which we hold and adore, offer upside potential but no capital returns in the case of the former and rather inconstant capital returns in the case of the latter. It's quite clear to us, as amongst our industrial holdings, TGP offers the best risk/reward relationship.

Even if Mr. Market fails to appreciate TGP's distribution yield, the company is likely to keep deleveraging or strengthen its stock buybacks if it remains depressed against its financial growth. In the meantime, we are getting paid a hefty dividend to wait.

On the preferreds

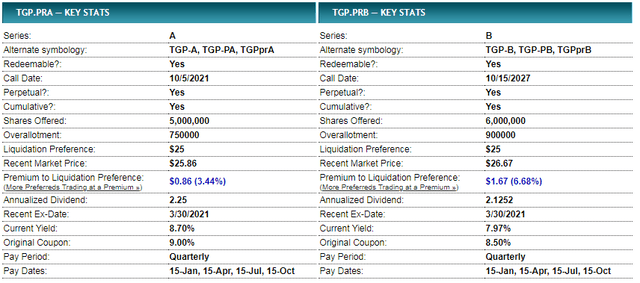

TGP has two outstanding preferred series, Series A (TGP.PA) and Series B (TGP.PB). You can clearly see their characteristics in detail below. Both are cumulative, perpetual, with original yields of 9% and 8.5%, respectively.

Coverage of the preferred dividends is hardly worth discussing, as adjusted net income shelters the preferred payments multiple times. Amid their safety (as it is also the case with various other shipping preferred stocks,) both Series A and Series B trade at a premium to their par value.

As you can see, since Series A's call date is rather close, and TGP is not unlikely to call them to save some additional financing costs. Hence, the market has priced the stock at a premium in which if one was to buy today, they would mostly break even (the capital losses would partially offset the upcoming dividends amid the lower liquidation price).

On the other hand, while Series B's call date is more than 6 years away, which means that investors will have plenty of time to accumulate dividends before getting redeemed, Mr. Market has priced the stock at a much more substantial premium. In this case, total dividends received will outweigh the capital losses from a potential redemption at the call date, but the current yield of around 8% is quite compressed.

If the company does indeed redeem this series on 10/15/2021, annualized returns will be slightly lower than the current yield, as well, due to the current premium paid. We don't think Series B is worth our money, though we can see some very conservative income-oriented investors appreciating its high safety and still substantial dividend potential.

Conclusion

While poised to grow significantly over the next couple of years, the Industrials sector features high valuations, which have priced in much of that growth already. Despite that, the shipping industry seems to be remaining relatively fairly priced, even though it has also rallied quite extensively over the past year. One of the stocks in this industry and amongst our holdings, Teekay LNG Partners L.P., has stood out, offering a superior investment case.

Combining the recent dividend increase lifting the yield to nearly 8%, its ample coverage, and the stock's inexpensive valuation make for a fantastic investment opportunity. We believe the stock is undervalued at its current levels, while its short-term upside is strong amid a potential valuation expansion. The sky-high dividend makes for a great stream of tangible returns as well, as we wait for such an expansion to materialize. Hence, TGP is our top pick for the rest of 2021 in the Industrials sector.

My co-pilot for running Wheel of Fortune, The Fortune Teller, will follow up on this article, with his next sector coverage.

So stay tuned to him, stay tuned to this series (we hope to cover as many sectors and top picks as possible), and stay tuned to the below special offer.

It's Wheel of FORTUNE's 4th anniversary, and we want you to be part of the celebration.

Subscribe before the end of April to a 4-year special plan:

1st year: $799 ($400 off)

2nd year: $899 ($300 off)

3rd year: $999 ($200 off)

4th year: $1099 ($100 off)

Only starting the 5th year, you'll pay the current-full $1199 yearly fee

Please visit the landing page, and go over the reviews before taking advantage of our 2-week free trial.

I hold a BSc in Banking and Finance. Here, on Seeking Alpha, I cover a variety of growth stocks and income stocks, including identifying those with the highest expected return potential, and a solid margin of safety.

Currently contributing as Promoting Author to the "Wheel of Fortune" marketplace.

Feel free to contact me at any time, and follow me here on S.A. for regular content and updates!

Happy investing!

Nick

Disclosure: I am/we are long TGP, STNG, DHT. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

This is one of those companies that, while I appreciate an almost 8% yield, I can't help but believe would be better off redirecting some of those dividends to paydown of debt and/or shoring up liquidity. Their cost of capital is high enough that cash used for debt reduction would improve their bottom line while making their balance sheet much more hiccup-proof.

@EdT.cpa_Retired Last year, through debt retirement, TGP reduced their annual interest expense by $25 million! That's $25 million that will not be an expense this year, and now drops to the bottom line. As more debt is retired interest expense will continue to drop and earnings rise. Management now also has the option of retiring units if they want to, or continue to raise the distribution. All options which favor unit holders. Very long TGP, and DRIPing. The editor of this article has picked a clear winner.

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Wow, Biden se compromete a reducir las emisiones de CO2 a LA MITAD para el año 2030.

Quizá sea puro parloteo. Pero si se llegase a cumplir significaría un tremendo golpe para la industria petrolera y gasística. Y un gran empujón para Tesla.

Lo que está claro es que la transición energética coge fuerza. Al menos hasta 2024, porque si gana Trump enviará todos estos planes a la basura.

#116077

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Analyticss

el bastion del oil (USA) se esta desmoronando, es verdad que es de ser iluso que pase de la noche a la mañana, pero si USA que es un mercado muy dinamico, le da por cambiar, podria hbaer una caida percapita del consumo de oil mas rapida en el tiempo, que los analistas hayan planeado. (dicen sobre 2027)

muchos analisis sobre demanda futura de petroleo se han realizado con la escasa o nulo, apoyo de USA a dichos proyectos por la era Trump, pero haber que pasa con los 4 trillones de dolares impresos y esos planes sobre la mesa.

Se que no es muy popular hablar de esto en este foro, pero se puede ver cosas como que los negados en la meteria vivan similar a lo que paso en negar a la tecnologia alla por 2015 y decir que esta cara y es una burbuja, solo porque los gestores lo decian.

No se yo hasta que punto, aqui hay un sesgo de confirmacion tremendo, con lo no-ESG.

Se van a poner trillones de dolares y de euros, en materia de ESG para los proximos 5 años, algo que hace 2 años, ni si quiera el mas ecologista del mundo, podria haber contemplado. mucho ojo y no perder de vista los cambios.

Yo si que considero un error negarlos , quizas la mejor forma, y digo quizas, de invertir en carbon/oil de los proximos 5 años, sera por costes, y no por volumen,

#116078

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Analyticss

hay que tener cuidado con el sesgo de confirmacion... y con nuestros gestores...

no vaya a ser que como en el pasado, nuestros gestores value fueron los ganadores de la guerra entre la tecnologia y el value.... en el futuro, no vaya a ser que los gestores ganadores sean los Value - ESG y los grandes perdedores los value no-ESG

de todas formas, buscar lo que nadie quiere, tambien implica encontrar mucho valor enterrado... ahora bien, que los gestores patrios esten a la altura, eso es otra cosa.

porque si por seguir el no-ESG, hay que buscar valur en empresas de paises EM,.... cuidado que uno se esta metiendo en paises que funcionan diferente y se la suda el mercado internacional.

#116079

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

BCN tiene una burbuja importante, toda la razón.

#116080

Re: Cobas AM: Nueva Gestora de Francisco García Paramés