Esa es la principal hipótesis de la tesis de Nick First. Te dejo su articulo en SA, para los que no tengan acceso. Que el rescate va a llegar de un modo u otro está claro, a AF no le interesa que NM caiga, aunque ella gana en todos los escenarios ya que es una de las principales acreedoras de NM, además de accionista.

El descuento es evidente que es merecido, pero si se confirma la tesis bullish en dry bulk yo creo que veremos a NMM muy muy arriba en unos años y la mayor beneficiada será AF.

Navios Holdings Buyout Could Unlock Massive Value

I have been trading and stock picking my way to outsized gains for more than 10 years. My investment background has evolved from early beginnings as a day trader, to swing trader, to my current state as a deep value investor who looking to build positions that have the potential to make outsized returns for the longer term. For all investment ideas I consider both the underlying equity and a variety of options strategies to find the best risk/reward potential.

I have expertise in the ocean freight sector and have been trading it actively for over 10 years. Other sectors I have extensive knowledge of include energy and alternative energy, basic materials, consumer tech, packaging, and all things China. My knowledge of the last two categories comes from a career running a packaging company with sales of over $100 million and over 100 days spent in China doing business there.

My strategy focuses on misunderstood names and industries, supply/demand imbalances as they develop, and paradigm shifts that Wall St is slow to pick up on. My strategies are data driven with often exhaustive due diligence. I build my investment thesis top down eventually narrowing to exploit the security with the most extreme risk/reward imbalance within the chosen sector. I would call many of my strategies high risk as I am generally searching for higher returns than can be found in low risk situations. Summary

Navios Partners has been frenetically issuing new shares and raising capital for an unknown reason, causing much speculation about a major impending related party transaction.

Due to a very strong dry bulk market, parent company Navios Holdings is back to a positive net asset value and is expected to be profitable next quarter.

A Navios Partners buyout of parent Navios Holdings would allow the combined entity to use NMM's balance sheet to refinance NM debt, cutting interest expense in half, unlocking big value.

An all-shares buyout would nearly double the size of NMM for a mere 8% net issuance of new shares and be immediately accretive to NAV and EPS metrics for NMM shareholders.

Photo by MAGNIFIER/iStock via Getty Images

For those of you that have been following the ongoing Navios empire saga, it has been quite the ride! Navios Maritime Partners (NYSE:NMM) has transformed into a cash machine in the past 9 months on the back of strong dry bulk and boxship markets as well as a very shrewd and well timed acquisition of daughter company Navios Maritime Containers (NMCI).

Despite a logarithmic rise of NMM share price, it remains HIGHLY undervalued and is especially so after a recent sell-off of shares on news of NMM already exhausting its $75M at-the-money offering and initiating a new larger $110M ATM. Shareholders are rightly concerned as share issuance at a fraction of intrinsic value reduces the upside case unless that cash is put to work buying assets at equal discount to intrinsic value. Anything less gives credence to a narrative that Navios Management is more concerned with expanding the fleet and paying related parties management fees than with creating shareholder value.

With around $365M of operating cash generation expected in 2021 and another $450M expected in 2022 (enough to easily grow the fleet by more than 50% organically), it begs the question: What opportunity is so large and urgent that NMM must raise $185M of additional cash over the course of just a few months? I believe that the answer lies with the springing maturity in September of this year on $305M of Navios Maritime Holdings' (NM) senior secured notes which if not remedied or refinanced will force NM into bankruptcy.

NMM could continue buying NM ships piecemeal at market prices leaving NM a shell of a company without assets that at best narrowly escapes bankruptcy or it can take out NM in its entirety in one big bite at its current distressed valuation, refinance the expensive debt load to a fraction of the cost, and unlock significant shareholder value in the process. I believe the latter scenario to be a distinct possibility as it checks all of the boxes for both management and shareholder interests. Whether taken as a whole or as part of a bankruptcy restructuring, I'd like to demonstrate that NMM is in a unique position to acquire NM assets at pennies on the dollar.

NM trades at a distressed valuation that matches market expectations of bankruptcy

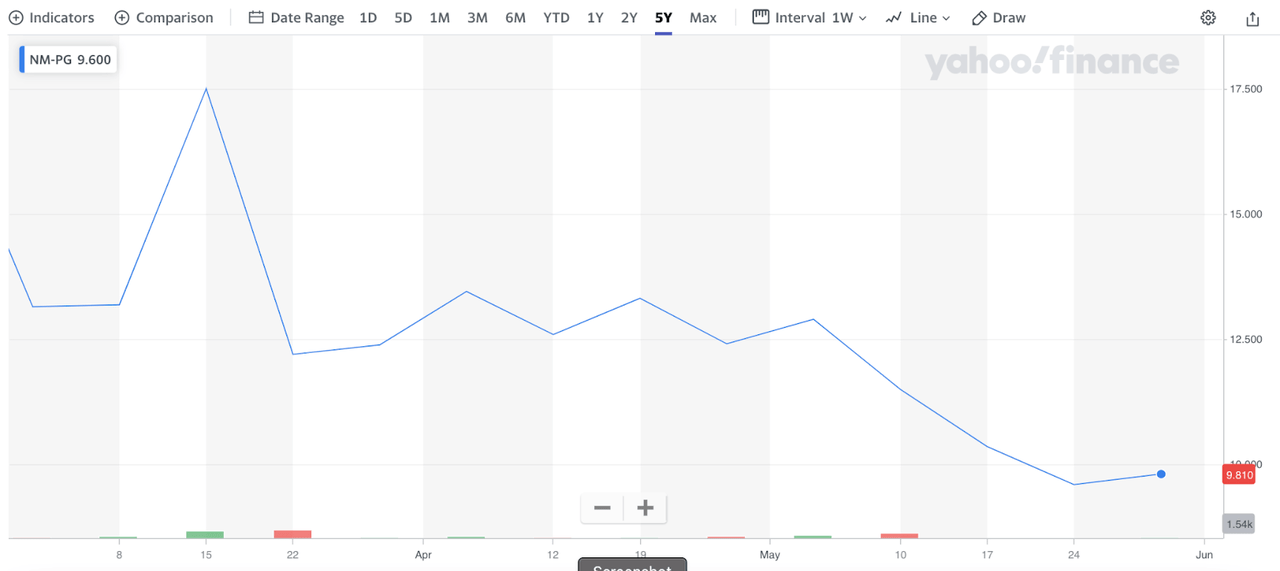

The best indication we have on market expectations for NM to survive its impending September springing maturity on $305M of debt and subsequent $476.8M balloon in January 2022 comes from the pricing on its preferred shares:

(source: Yahoo Finance)

The preferred shares trading at less than a third of par value plus dividends in arrears implies that the market expects less than a 1/3 chance of survival and repayment.

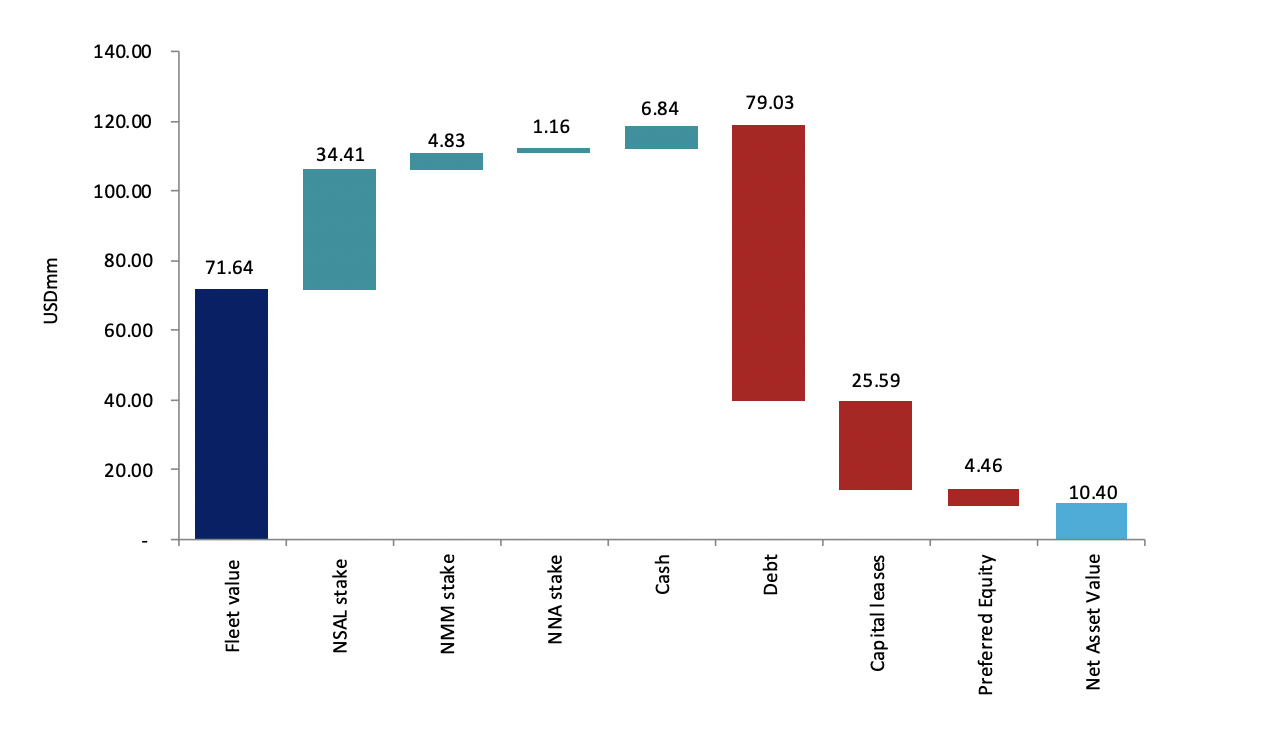

Meanwhile a recent upsurge in dry bulk earnings and underlying asset values has led to NM common shares returning to a positive net asset value (NYSE:NAV) of around $10.4 per share according to an April dated Clarksons research report:

Source: Clarksons

Source: There is much debate and a big asterisk on Clarksons' NSAL stake valuation as this is an illiquid asset that is hard to value. NM is pursuing an NSAL IPO so we may get more clarity on this value in the near future, but for the purposes of this analysis, we will use the Clarksons estimate.

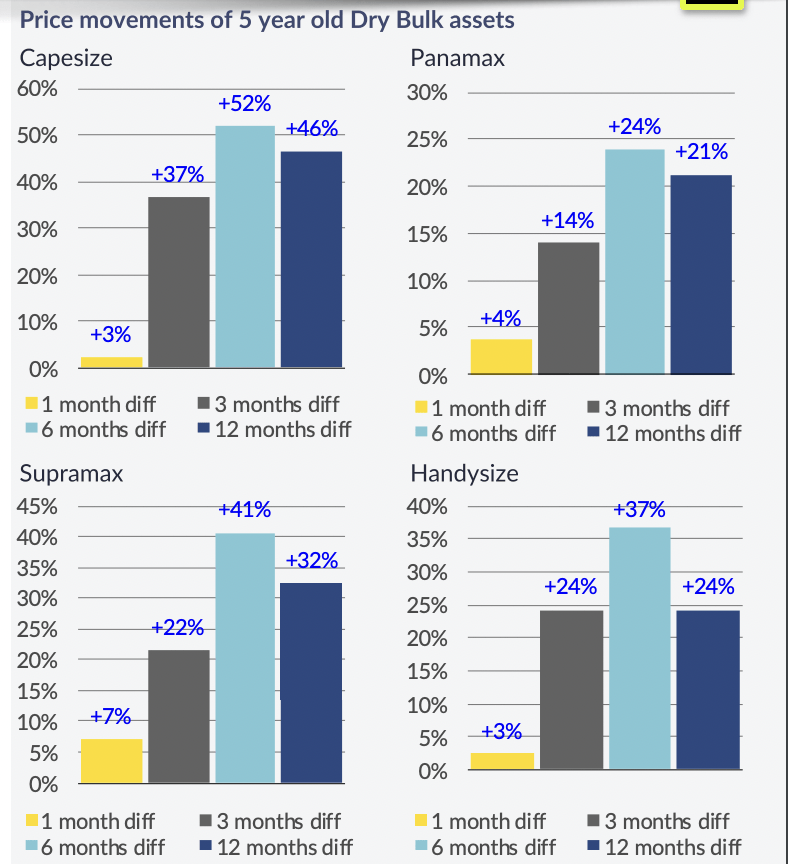

Asset values have continued to rise since April seeing gains of 5% or more:

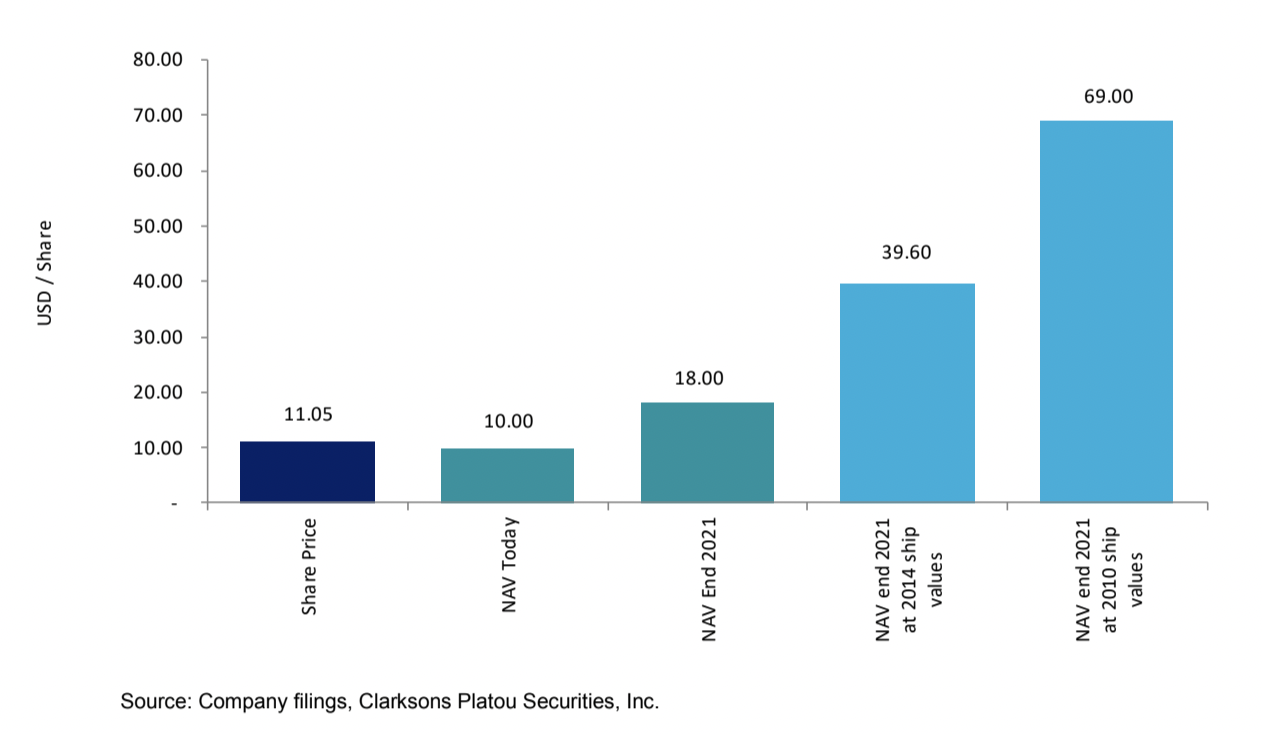

Every 10% gain in asset values represents an additional $7 of NAV per share on NM shares. My best guess for NM NAV at time of writing is around $15 per share. Should we return to 2014 or 2010 asset values, Clarksons estimates NM NAV per share would rise to $39.6 and $69 respectively:

With dry bulk rates at decade highs, and both newbuilding and steel prices soaring, it seems only a matter of time before we reach 2014 asset values and start making our way toward 2010 asset values, meaning that there is a strong possibility that NM NAV will be closer to $50 per share in short order.

With the September springing maturity looming and very little hope of NM refinancing and preferred share prices indicating a likely bankruptcy, it is no wonder that NM common shares are trading at a significant discount to Clarksons NAV estimate and arguable liquidation value - it's just not worth the risk of seeing what happens in a bankruptcy restructuring.

Even with massive interest burden NM expected to a cash machine in coming quarters

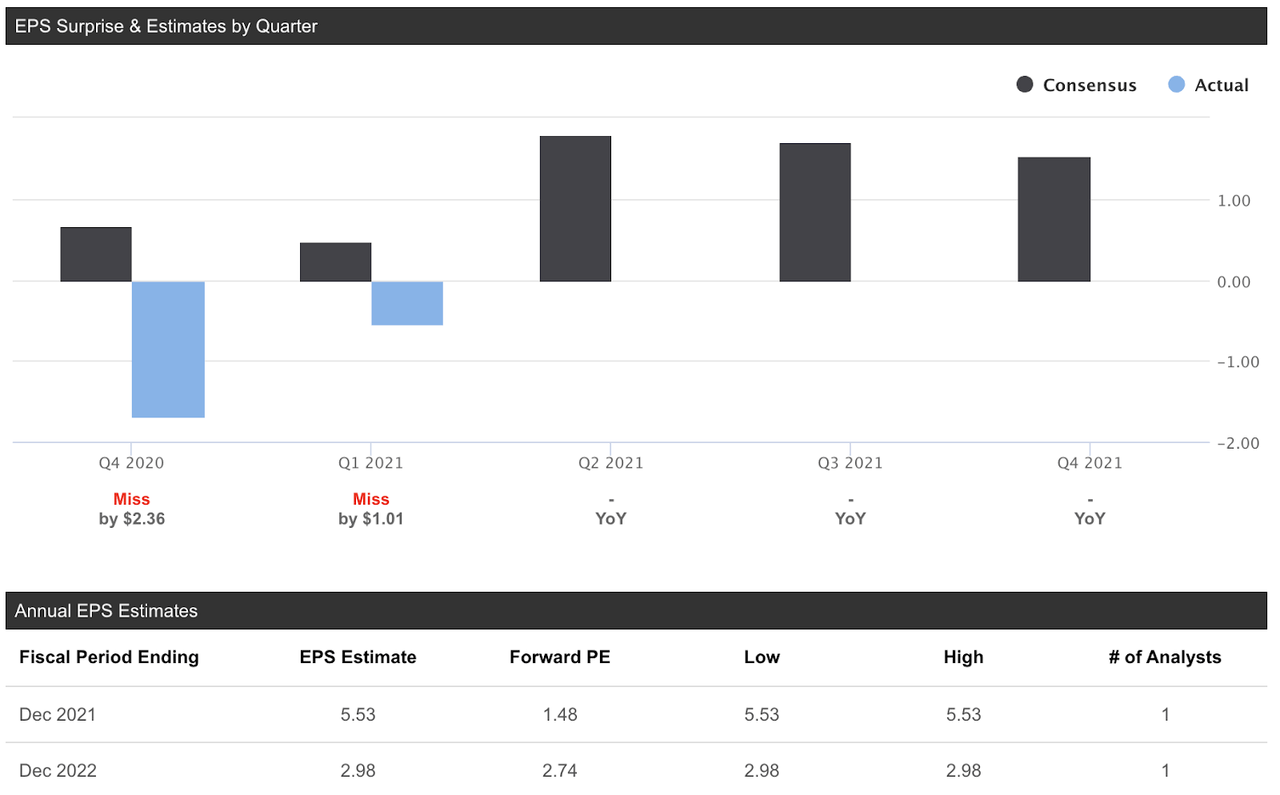

According to Seeking Alpha, the one analyst (Clarksons) covering NM expects NM to earn $5.53 per share in 2021 and $2.98 per share in 2022:

NM is trading at an absurdly low 1.48x 2021 estimated earnings as investors judge bankruptcy probability as far too high to justify the risk. What is most amazing about this estimate is that it comes despite a trailing 12 month interest expense of $136.6M at an effective interest rate on NM debt of 9.1%. Compare this to a sub 4% effective interest rate on NMM's debt. If NM were able to refinance this debt at NMM rates, it would contribute an additional $70M+ per year or $4.4 per share of net income. At NMM's debt cost NM would make about $10 per share in net income in 2021 vs its current share price around $8.

If only there was a way for NM to survive bankruptcy and refinance its debt to rates in line with NMM's, its shares would be worth many multiples of their current value!

Enter NMM, its fortress balance sheet, cash pile from recently consummated ATMs, and massive contracted cash flows

After completing its recent $75M ATM and implementing $110M ATM plus adding $85M of operating cash in Q2, NMM will be sitting on a $319M mountain of cash. Q2 ending net debt to book capitalization will be just 22%.

If NMM were to buy out NM in its entirety in an all-shares deal and absorb all of its debt, it would still have a very manageable 58% net debt to book capitalization which could very quickly be reduced to just 33% by 2022 end after its massive expected cash flows in the coming 18 months:

NMM buyout of NM immediately accretive to NMM EPS after debt repayment and refinance

Now that I have demonstrated that NMM can fairly easily digest NM from a leverage perspective, let's look at what the implications are from an earnings per share metric:

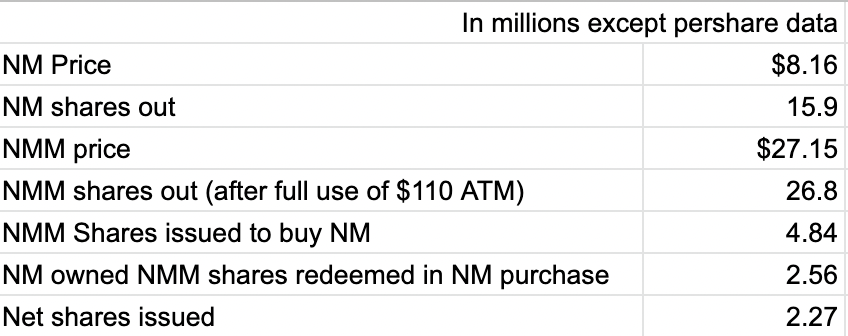

If NMM were to buy NM, I would expect it to be an all-shares deal as Navios management has shown from the recent ATMs that they prefer to have cash rather than a low share count. The NMM shares issued however would be mostly offset by the 2.5M NMM shares owned by NM that would be redeemed with the purchase reducing the net shares issued to around 2.2M or a less than 10% additional dilution:

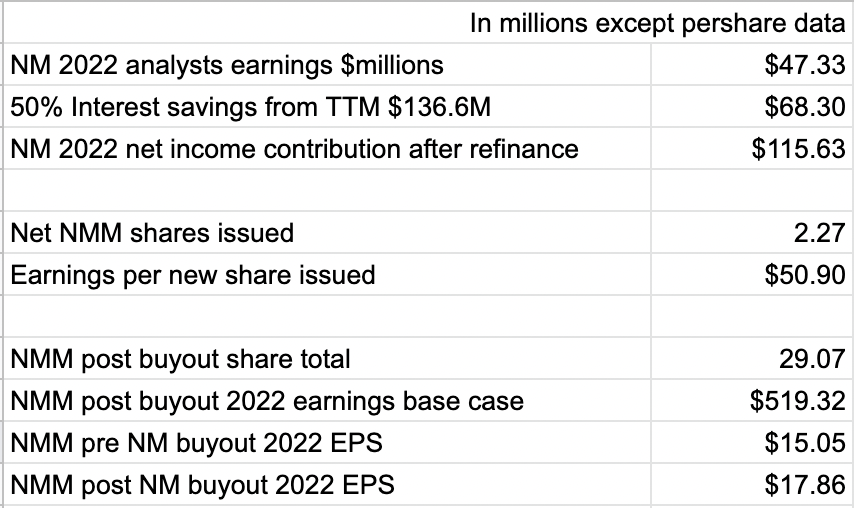

In exchange for the 2.2M shares issued NMM would likely generate more than $100M of additional net income per year from NM assets after refinancing and using its cash pile to pay down NM debt:

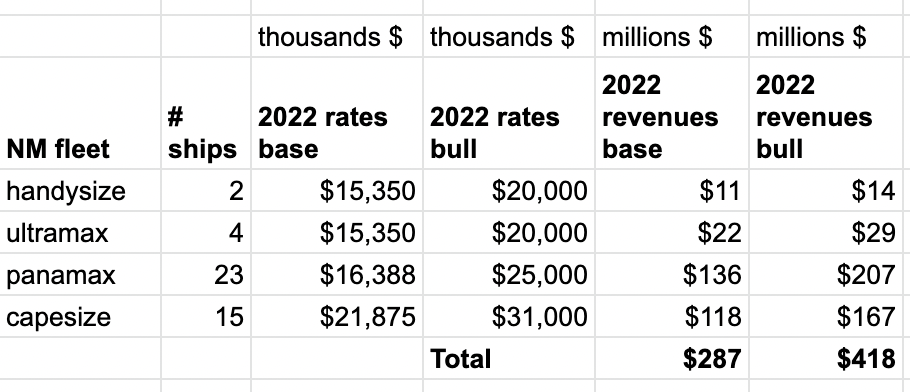

My back of the envelope math reveals a potential massive $50 per share net income contribution per newly issued NMM share in 2022, increasing expected EPS for on the entire NMM share base from around $15 to nearly $18. That is a 20% increase in EPS on a less than 10% net new share issuance. And that is on the Clarksons 2022 estimates plus refinance savings which I believe to be a bit dated and far too conservative. My base revenue case based on 2022 FFA market rates actually shows higher revenue than Clarksons is forecasting:

(source: Author's Model based on company filings, FFA rates, Author's estimates)

If 2022 sees the types of rates we are seeing in 2021, as I expect it will due to a very thin newbuild orderbook, I expect an NM purchase would contribute an additional $240M of net income to NMM in 2022. This is about $4.5 per share more than the Clarksons estimate and takes my bull case EPS for NMM to over $22 for 2022.

Bottom line: If NMM were to buy NM in an all-shares deal, and dry bulk rates in 2022 simply match those currently expected for 2021, the new much larger NMM would make around $22 per share in 2022 implying a 2022 PE ratio for the new NMM of just 1.3x 2022 earnings.

A much larger NMM would fetch a higher valuation

NMM is already the 3rd largest publicly traded dry bulk company on a number of ships and deadweight ton basis with 89 ships totaling 6 million DWT of bulkers and another 2.2 million DWT of boxships. The NM fleet would add 43 ships and 4.8 million DWT. Combined, it would have 132 ships and 13 million DWT. This compares to the largest publicly traded drybulk company Star Bulk (SBLK) with 128 ships and 14.1M DWT. A combined NMM and NM would actually have more ships than Star Bulk and similar fleet carrying capacity.

NMM's market cap after absorbing NM via an all-shares deal would be a mere $725M vs SBLK's market cap of $2 billion. NMM share price would need to triple to match its nearest peer with the closest fleet size and profitability level. Although I expect NMM to continue to trade at some level of discount on corporate governance concerns until management can prove they will return capital to shareholders, I expect NM to close the gap at least halfway maintaining a 33% discount to SBLK which would represent a doubling of NMM share price from here. Should NMM increase the dividend or buy shares, I would expect the gap to close further.

Angeliki Frangou has $30M+ reasons to avoid a NM bankruptcy

President and CEO of NM Angeliki Frangou (NYSE:AF) owns 25.4% of NM according to the latest filing. This is more than $30M worth of NM stock at current share prices. If NM is allowed to slip into bankruptcy this stake is worth $0. If exchanged for NMM stock, this $30 million is easily worth $100 million to AF if management interests become aligned with shareholders and NMM initiates a favorable capital return policy. I think shareholder-friendly capital return is a much more likely possibility if AF has significant direct ownership in NMM rather than indirect ownership via a failing NM. Other reasons the Navios management would want to save NM include:

AFs Navios Ship Management (NYSE:NSM) affiliate company loans would be repaid in full.

Navios keeps every NM ship (including chartered ships) under the Navios umbrella and actually upgrades management fees as NMM pays higher rates than NM.

Very defensible and what I argue to be a very favorable outcome for ALL parties involved.

NM debtholders, preferred holders, and common holders all get bailed out.

NMM shareholders pick up NM assets for pennies on the dollar.

Removes the urgency for NSAL to IPO, allowing NSAL shareholders to get fair value at the right time in the future.

Avoids an ugly reputation black mark with capital markets, allowing Navios to maintain strong relationships with creditors.

History has told us to expect actions that align with Navios management interests. I believe a NM buyout to be a strong possibility because it aligns best with management interests and just happens to also be a good deal for shareholders in a strong dry bulk market.

Distressed NM assets are on sale for pennies on the dollar, and NMM is the only potential buyer

NMM bailing out a failing NM was once a nightmare scenario for NMM shareholders as it was far too big and far too leveraged to digest. Things have changed thanks to very strong expected earnings at NMM and the massive cash pile it has built for itself already. Putting the pen to paper reveals that buying NM in its entirety would actually be fairly manageable for NMM to digest and an opportunity to buy assets for pennies on the dollar at the start of a bull market in drybulk. NMM just happens to be the only entity out there that could pull this off, putting it in a unique position to create serious value for its shareholders while also checking all the boxes for management.

Although this is pure speculation on how NMM's cash pile may be put to use, modeling a direct all shares buyout has been an excellent exercise to really understand what is possible. There are many other ways NM could be restructured, all of which I expect NMM capital will participate in. I expect any major deal announced will be at least as accretive to NMM shareholders as the possibility modeled here as NMM is in the unique position of having a massive amount of capital on hand to deploy and a common management to facilitate a transaction that would otherwise be too messy for a 3rd party.

I am now fully hoping for an all-shares buyout offer of NM from NMM. It is a transaction that I can understand and one that I believe will create massive value for NMM shareholders in the coming years. It also removes the NM overhang and uncertainty that is holding NMM shares down and aligns management with shareholders through direct ownership. At the very least I believe this should represent the baseline return expectation for NMM's cash pile once put to work meaning that whatever happens we should see NMM EPS of $18-$22 in 2022 vs about $15 per share if the cash just sits on the balance sheet. This means that NMM is likely trading at a 2022 PE ratio of just 1.3x-1.6x even with the higher share count from both ATMs being fully utilized. Although I completely understand the recent sell-off based on unfriendly dilution and uncertainty regarding both future dilution and use of the proceeds, I believe the sell-off to be overdone with the distinct possibility of a highly accretive transaction coming down the pipe.

Nothing has materially changed about my thesis that NMM remains the best risk reward buy out there at an absurdly cheap valuation. If you have not been following my series of articles on the subject and are coming to NMM for the first time, you can find more in depth explanation on why I believe we are at the beginning of a supercycle in boxships and dry bulk and why I believe NMM to be a multi-bagger from here on my article page.

Se está hablando de:

Cobas Internacional

Gestión activa

Value Investing

El objetivo del equipo de inversión es construir una cartera “long-only” diversificada.

Gracias, lo conozco porque desde hace años sigo la saga de la famiglia Navios.

Los datos objetivos es que AF ha sabido ir aguantando y manipulando por aquí y por allí durante los últimos 5 años, hasta que se ha encontrado un ciclo de dry bulk descomunal que le está sirviendo para ir rescatando poco a poco a NM.

Hasta hace poco, NM no era viable ni para refinanciar. Ahora lo será para refinanciar pero esa deuda no la podrá pagar con el tiempo.

Estoy de acuerdo contigo en que falta poco tiempo, en Sept'21 es la refi de 305m$ de NM. Ahí tendrán que poner las cartas encima de la mesa.

Esperar o argumentar a posibles resultados de 2022, lo veo muy peligroso. No lo tengo estudiado pero me resulta curioso que se piense que el superciclo de dry bulk es algo estructural y va a durar unos años.

Freedom is driven by determination

#126091

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Al final, cómo sabes, todo depende del orderbook y de que no se caiga China. En este momento además tenemos dos ingredientes extra que serán: con seguridad las disrupciones causadas por las nuevas regulaciones que no sólo afectan en forma de bajada de velocidad sino como incertidumbre de cara al futuro. Y como extra los planes de estímulo coordinados que supuestamente veremos los próximos años.

En cuanto al orderbook. Este es el panorama: Estamos en mínimos históricos y con los slots de astilleros a tope de pedidos containers y LNG. Además que los bulkers son los que menos margen dejan a los astilleros, con lo que mejor incluso. En los próximos años todos esos barcos del boom de los 2000 se verán obligados a reducir velocidad por las regulaciones lo que apretará todavía más el equilibrio oferta/demanda.

Si vemos como ha evolucionado el Baltic dry: Se puede ver que la tendencia ha ido mejorando desde 2016, con las excepciones de: el colapso de Vale en enero de 2019 que provocó una bajada muy fuerte sostenida al disminuir muchísimo las toneladas entre Brasil y China ese año. Y la bajada de principios de 2020 de Covid.

Este año el guidance de Vale es mucho más fuerte para H2 que para H1, con lo que se espera una segunda mitad de año al menos tan buena como la primera.

Este es un negocio nada especial, en la última década ha sido un destructor de capital enorme, pero creo sinceramente que los próximos años deberían ser muy diferentes. Si vemos un desequilibrio duradero entre oferta/demanda podemos ver retornos brutales, no diría similares a la década del 2000. Pero si muy buenos retornos.

Estos días Troim levantaba pasta para crear un nuevo vehículo además de 2020 Bulkers:

Tor Olav Trøim is getting back into dry bulk, saying he sees similarities between today’s market and the supercycle days of 2003 to 2008.

Trøim is creating Himalaya, a dry bulk owning vehicle which has an initial outlay of $800m to order 12 newbuildings, according to Oslo-based newspaper Finansavisen.

“This is very reminiscent of the structural upswing we saw in shipping between 2003 and 2008,” Trøim told Finansavisen, discussing the current supply and demand situation in dry cargo .

Trøim said the Himalaya name had been chosen because the bulk market looks very exciting now.

Trøim chairs Golar LNG and is a director at Borr Drilling. Previous exposure to dry bulk came via Golden Ocean and his many years working with John Fredriksen after which he went on to found 2020 Bulkers.

Los barcos creo que se los entregan en 2 años, creo que si no lo viese claro no tendría necesidad de meterse aquí teniendo ya exposición.

Entiendo las reticencias porque es un sector en el que si las cosas salen mal, salen muy mal. Y todavía las entiendo más con NMM porque es de lo más peligroso del sector. Pero creo que el momento es bueno, obviamente me puedo equivocar y si lo hago no será barato 😅

#126092

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Es una caída generalizada Genco y Eagle están cayendo más todavía. Oil, carbón, gas, oro, lleva todo cayendo con ganas unos cuantos días ya a pesar de que los fundamentales sigan ahí. El oro en el último mes ha caido un 2% y algunos productores han caído un 25%. Con el oil pasa lo mismo, está a niveles de hace un mes y las equities llevan correciones del 20% en muchos casos.

En otros sectores es parecido, desde el mensaje de… está todo controlado, es todo transitorio el mercado se ha girado con fuerza. Veremos lo que dura, porque ya digo en muchos sectores no ha cambiado nada. No se si las dudas con la variante Delta están influyendo…

No creo que haya terminado el ATM, espero que no estén vendiendo a estos niveles, pero tampoco lo descarto.

Yo llevo una buena corrección en mi cartera, me salvan las primeras posiciones que me aguantan bien pero en lo demás la hostia está siendo buena. Veremos en unos días que tal sientan las presentaciones de resultados.

#126094

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Desde el momento en que a AF le importa una mierda la cotización de NMM, o al menos le importa menos que levantar los 110m$, creo que tiene una orden con un borker para vender el 20% del volumen diario. Así, a pelo y sin distinciones.

Si me la ponen bien para trading la meto un mordisco. Pero con cuidado.

Freedom is driven by determination

#126095

Re: Cobas AM: Nueva Gestora de Francisco García Paramés