Cobas AM: Nueva Gestora de Francisco García Paramés

Página

17.085

/

19.072

#136673

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Yo sigo dentro.... Es normal que no caiga mucho tampoco, ahora se valora por el dinero que va a sacar de TGP. Donde antes había deuda ahora va a haber caja neta. Otra cosa es que anuncien plan de inversión, que se pongan a comprar barcos como locos y no guste a los pocos inversores que todavía confían en ellos, entonces la veremos a 2$ o menos...

Se está hablando de:

Cobas Internacional

Gestión activa

Value Investing

El objetivo del equipo de inversión es construir una cartera “long-only” diversificada.

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Pero también influirá mucho el devenir del sector en ese contexto. Entonces, si coincide con una zona del ciclo Down y encima no gusta el nuevo plan se puede ir a 1. Pero eso son dos factores negativos que tienen que coincidir. Ya sabemos que las dos cosas interfieren en el precio pero que si las noticias malas no son tan malas y el ciclo ayuda pues la cosa cambia. Me gustaría saber la opinión de @silvermoon , no sólo porque sabe mucho del tema sino porque personalmente es uno de los que más se juega.

#136675

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Lo del goteo de TK me refiero que el dia de la noticia se pudo vender sin problema a 3,90 al dia siguiente a 3,75; yo pude vender a 3,60 y hoy ya va por 3,40

Cada día que pasa baja un 1-2%. Es posible que se estén saliendo manos fuertes sin tirar demsiado el precio, todos los dias se duplica el volumen medio.

#136677

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

sobre la OPA de TGP, ¿alguien tiene claro de cómo se mueven realmente estos temas en EE.UU, o no sé si decir en Bermudas o las islas Marshall? Yo tengo acciones de una empresa inglesa, en la que una especie de Private Equity que ya controlaba una parte gorda comprada a los fundadores unos meses antes (el PE tienen un 30% y los fundadores se quedaron otro tanto), anunció en junio que quería comprar toda la compañía mediante una OPA al mismo precio, y al final, no ha salido adelante, parece que por la oposición de los consejeros independientes (los miembros del consejo de administración que no son accionistas) que dijeron que el precio no era suficiente. ¿no existe ese papel de consejeros independientes en el consejo de TGP? Me parece que por el hecho de que esté incorporada en un paraíso fiscal y legal desgraciadamente van a hacer lo que quieran.

#136678

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Si, ya le leí eso, pero es evidente que ese día estaba en caliente y aunque ya dijo muchas cosas no ha vuelto a decir nada más ya un poco más en frio con el paso de los días.

#136679

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Golar y Gabriel

The Best Is Yet To Come

May 19, 2021 4:30 AM

The last year has been very difficult for the company but Golar has always come up with an alternative to deal with those temporal problems.

Environment has dramatically improved. The likelihood of new FLNG projects greatly meliorated based on the new level of the LNG.

I am convinced that Golar is to date worth around $25 and could potentially be worth up to $100 by 2030.

One year has passed since my interview. If we look back on the last year it was a very difficult one for the company. On the one side, we have seen the MLP, being Golar the General Partner, reducing the dividend to have success in the bond extension, the Gimi force majeure, the Hygo IPO cancelation, the shareholder class action, the CEO resignation and the equity raise. On the other side, we have good news too. Golar has always come up with an alternative to deal with those temporal problems. They delivered Viking to Croatia on time and on budget despite Covid issues, they dealt successfully with BP/Kosmos and the suppliers in the Gimi force majeure, they sold the MLP business at a fair price knowing that this type of structure is dead, the putative class action lawsuit filed against the Company was dismissed and finally, they managed to strengthen the balance sheet divesting Hygo to New Fortress.

Despite the amazing ride the stock has experienced since our article, I consider the stock cheaper today than then. This paper will attempt to show my thoughts on the events that have occurred and furthermore I will explain why I believe that Golar is a very compelling investment opportunity for the coming years. I am convinced that Golar is to date worth around $25 and could potentially be worth up to $100 by 2030.

As stated in Golar's press release last 15 April 2021, Golar completed the sales of Hygo Energy Transition and Golar LNG Partners. Golar received $50 million in cash and 18.6 million common shares in New Fortress Energy (hereinafter referred to as NFE) worth $878 million based on the April 14 closing price as consideration for the sale of its 50% interest in Hygo. It is noticeable that Golar now owns 9% of NFE which is likely to become the biggest downstream LNG company in the world. Moreover, Golar received $81 million in cash for the sale of its 32% interest in Golar LNG Partners (hereinafter referred to as GMLP). The company is making efforts to simplify the business structure in order to make its value more evident. Golar has been de-risked and simplified as the valuation of its downstream business is now directly visible in NFE stock.

I have to admit that the Hygo sale is not my dream deal, but I am glad that Golar has found a solution and has not given an inch to external pressures. Moreover, I am happy to see Golar sharing the downstream business with Wes Edens, the NFE CEO. Together, both companies have created the best downstream LNG company with a unique solution to deliver cheaper and cleaner energy to the emerging market. Furthermore, Hygo deal has reduced the risk of refinancing the convertible maturing in February 2022 through either a refinancing into a new convertible backed by some NFE shares or a straight secured bond applying NFE shares as a collateral. I expect Golar paying a small part of the convertible (~$50M) and refinancing the remaining part into a new convertible that will be exchangeable to 5M of NFE shares (slighly up or down, depending of the NFE shares at that time) while retaining 13.6M shares. I think Tor Olav Trøim believes in the long term NFE prospects, so I will not expect Golar selling NFE shares anytime soon.

However, let me start by recapping how we have reached this point. Golar was going to IPO the Hygo business last September 2020 but it was suspended 24 hours before the IPO since the news of an investigation dealing with corruption were leaked. Hygo CEO, Mr. Eduardo Antonello, was being investigated for bribery (Operation Car Wash) regarding its implication in the deals between Petrobras and Sapura in 2011 and worth around $2.7 billion. Consequently, the Hygo chief executive resigned from his position and focused on pleading his innocence. It is worth to know that Brazil Operation Car Wash began in 2014 and radically changed the whole public tender process. I would say that the Brazilian power market is one of the most transparent in the world and Golar started its operation in Brazil long after that time, so we were very comfortable increasing our stake by that time.

Those news were an overhang to the Hygo business even though Mr Antonello’s has negated any involvement and no formal charges have been brought against him. To be honest, if this hadn’t happened, I would have preferred the IPO but it is fair to say that, after considering it all, it has changed the reality in the ground and I reckon the NFE deal is the best outcome. Also, those unfair claims required Golar to make a small equity raise to be compliant with bank covenants. Golar had a $180M loan that was expected to be refinanced with the Hygo IPO, so with that mishap, the bank wouldn’t take risks and required Golar to increase capital. However, we proved one more time that big shareholders are still supporting the company and the requested discount was very low.

Due to the extension, I will not analyze New Fortress in detail here, but I think the stock is cheap at the moment. NFE was trading at 34x 2022 EBITDA pre-deal. It is not secret that the stock was hot because the excellent management team, the amazing business prospects, and the hydrogen hype. However, after factoring Hygo and Golar LNG Partners businesses and partially including the recent announcements (two new more terminals and the Fast LNG business), New Fortress is trading at 12x 2022 EBITDA which I think is quite cheap considering the management excellence and business prospects. You should understand that NFE is a growth company going from none operating margin at all in 2019 up to $1.2bn committed and potentially up to almost $3bn annualized operating margin by 2023. I consider the stock fairly valued at $60/share but if they execute correctly its pipeline, it could be worth up to $100/share in the next few years.

I am aware the market does not consider Golar doing a good deal. Golar’s market value has become inherently linked to the NFE share price. The Hygo/GMLP deal explains more than 70% of the current price assigning very little value to the midstream and the disruptive upstream businesses. It makes no sense that the market believes that the remaining businesses are worth a bit more than $3 per share or $350M. The market has no clue of the Floating Liquefaction business prospects and I understand it as they haven't signed new deals for a long time. However, I would argue that the environment wasn't appropriate but it has dramatically changed in recent years.

In addition, I would highlight Golar focusing exclusively in its FLNG segment is a good deal. The downstream business in the hands of Mr. Wes and the midstream business not requiring much attention with most vessels on period charters allows Golar essentially just to concentrate on getting new FLNG projects.

This does not really concern me since only time will tell. I remember when Golar was trading above $30 by mid-2018. At that time, nobody cared about the downstream business. The market did not understand why Golar was investing money in that segment if the FLNG (upstream) business economics was better. Golar set up Golar Power (now Hygo) because the gas supply/demand break new ground in the downstream business and created a difficult environment for getting FIDs on liquefaction projects (upstream business). They saw the opportunity and associated with a financial partner (Stonepeak) because their balance sheet was not big enough to deliver those projects alone. As I said before, although the market did not fully understand, they correctly read the supply/demand dynamics and built a fantastic business from scratch that will generate a book gain of approximately $740M making 3.5x return on capital invested in just five years.

Once again, the market is one step behind Golar. It is time to invest in the upstream segment as I will justify below, but first, let me explain why the gas is essential. We firmly believe that gas plays a key role in order to decarbonize the economy, especially in emerging markets such as Asia, where the coal market share in the energy mix is above 60%. Natural gas is a bridging technology that potentially could become a permanent solution depending on the ability to remove carbon dioxide emissions in the transformation process. It is worth to know that Natural Gas fits best with the renewables. Renewables are by nature intermittent, dependent on the weather and not flexible enough to increase the generation at peak hours. While gas is sufficiently flexible to quickly cover those gaps, that is not the case with other alternatives such as nuclear energy. Moreover, gas is clean, cheap, abundant and easy to transport. That’s the reason why Asian countries are choosing gas in order to replace coal. Even during tough times, the LNG has grown in that region, for instance, Asia LNG imports grew by 3.5% in 2020 leaded by China and India with demand growth of 13.5% and 14% respectively.

Source: Berstein research: China gas demand estimates

While gas demand has been growing quickly, the supply has grown quicker and it has created excess supply growth that has kept the LNG prices depressed. Gas is not different than any other cyclical sector. As I use to say, the best remedy for a cheap gas is a cheap gas. The super cheap gas cycle we have experienced over the last years has accelerated the coal switching and has strongly reduced new capacity additions given the lack of new investments. We reckon on just 10MPTA of new supply increment during the next 4 years after 30MTPA of new LNG additions over the past 4 years, being just 3-5% of annual demand. In the same way, there have been a shortage of material LNG supply impacting on the market in consequence of LNG projects such as Prelude or Mozambique.

Source: Bloomberg

The price increase we saw last winter helped by La Niña was a warning. We see tighter markets ahead. With strong demand on a global economic recovery, limited new supply over the next years and gas inventories below its 5-year average, the economics give more sense to the upstream segment and also justify Golar’s last move.

Source: Golar LNG Q4 2020 earnings presentation

Golar has developed the most cost-competitive floating liquefaction solution. Golar’s FLNG model is a disruptive concept and able to access to low-cost reserves and deliver them to Asia at prices well below the U.S. land-based terminals (the lowest-cost producer). Golar has the cheapest and quickest solution successfully proven. The Hilli FLNG is the only one whose performance has been outstanding with 100% up time for two and a half years. However, we understand that despite Hilli is the lowest gas producer in the world, they can’t make things work with gas at $3/MMBTU in Asia. It is fair to say that we expected Perenco moving forward with the train 3 by this time, but COVID delayed it. With the current LNG environment, we expect Golar announcing Hilli T3 within this year. However, I am aware that Golar is not satisfied as showed during the last earnings call. Golar is not going to sit and wait and if they don’t have the full utilization and contract extension they require, they are going to reallocate the FLNG and increase the utilization. I believe that having New Fortress now on board will make easier to get Hilli fully operating as NFE owns part of the asset and it is a credible potential offtaker as executing Hygo backlog will require significant volumes of LNG. For example, Hilli is one of the closest sources of supply with cheap LNG and cheap shipping costs to supply the Barcarena FSRU.

I want to highlight my belief of Perenco’s making significant commitments to Golar sooner than later because I estimate there is enough gas for another 10/12-year contract at full capacity; therefore, if the Hilli FLNG leaves Cameroon, Perenco will lose the income stream because it will be extremely difficult to find a replacement. However, it is fair to say that Golar reallocating Hilli in another place is feasible. Golar would only need to invest $50-100M and it is important to know that the gap between the time Hilli will be disconnected from Cameron and redeployed and starting to make EBITDA is minimal, less than 12 months. Anyway, I expect Perenco increasing the Hilli utilization very soon and subsequently extending the contract that ends by mid-2026.

As you may now, Golar has two FLNG projects. The Hilli project, which is currently generating healthy and stable FCF and the Gimi FLNG, in which they are currently working and that was expected to be online by the end of 2022, but BP claimed force majeure and now it is expected to be in action by the second half of 2023. BP said that they couldn’t work on the project because COVID restrictions and managed to delay the project. Despite the delay, the project will be excellent for Golar, just with a 9-month postponement. I guess BP did not expect LNG prices recovering so quickly, so I guess they wish they have never pressed to delay the project. Well, we need to understand that retaining cashflows in order to maintain a healthy balance sheet was the priority during COVID times and nobody expected such a strong recovery on oil and gas prices. If one reads the last BP CMD, one will understand how important the LNG segment is for them. They committed to significantly increase the LNG portfolio up to 30 million tons of LNG by 2030 and the only way to achieve this is through the Great Tortue project. This project is a Kosmos-BP partnership developing an innovative near-shore liquefied natural gas (LNG) project in the Tortue field offshore Mauritania and Senegal that is among the lowest cost greenfield projects in the world. The initial phase of the project is expected to deliver approximately 2.5 MPTA of natural gas and it will employ the Gimi FLNG, but the partnership is also evaluating potential expansion up to 10 MPTA in subsequent phases. In fact, Kosmos and BP recently announced they will FID the second phase of the project during the second half of 2022 and probably it will be working by the second half of 2025. They are downsizing the second phase to 2.5MPTA in order to reduce the capex and leverage the infrastructure built in the first phase. If they had gone ahead with the initial project (3.7MPTA), they would not have been able to leverage the infrastructure and would need to invest more capex because, for example, the FPSO from phase 1 would not have been able to deliver enough LNG. Being said that, they are confident it will be a 10MPTA project as initially scheduled. It is important for BP and Kosmos to have the second phase online because the breakeven for first and second phases delivered to Asia altogether is under $5/MMBTU, however, the first phase breakeven is around $6/MMBTU and around $3/MMBTU for the second phase. We expect BP/Kosmos announcing a new Golar FLNG as Golar’s solution is more economical, more environmentally friendly (ESG) and it has not to be financed because it is opex for them, while the alternative requires tons of money expended as capex for BP/Kosmos.

As you may notice, we are super optimistic on the FLNG segment. Golar states they are in talks over 9 FLNG projects and in my view, the likelihood of those potential projects greatly improved based on the new level of commodity prices, so I expect at least 3 FLNG projects in the next 5 years. Also, we feel Golar has now the ability to finance them due to its better balance sheet after Hygo/GMLP divestments and the new financing conditions they have negotiated with the Korean shipyard.

Trading below $12/share, the company is not properly valued and we can see why the company is currently repurchasing shares. Golar is the perfect bet if you really believe in the LNG structural trend. According to my estimations, the company is worth $25 right now. Golar shipping segment is worth around $2/share including the FSRU (Golar Tundra) and the Avenir LNG which is developing small scale LNG infrastructure projects, while the downstream business is worth $10/share with NFE stock trading at $60 ($7/share taking today’s prices). Finally, the FLNG business (including the holding net debt) is worth $13/share. I would emphasize that I’m not taking into consideration any potential growth or the Floating Blue Ammonia segment. I consider Golar will increase its target price between 5 and 10 dollars with every new FLNG project.

I believe Golar’s stock price should continue to close the gap to underlying values. Catalysts could be getting new FLNG projects, selling a small stake in Gimi at fair multiples proving the market how good Golar’s assets are or the LNG shipping spin-off.

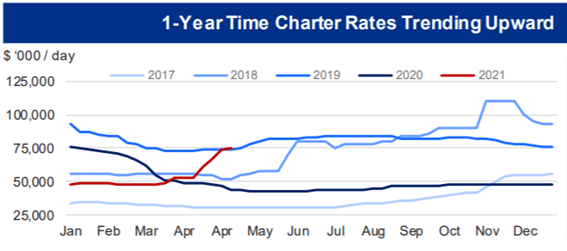

I assume this might sound odd and even unbelievable to you since Golar has been trying to carry it out for a long time but I feel the LNG shipping environment has changed. Fearnleys reported 1-year LNG rates at $100,000 by the end of April. It shows that the market is very tight. The LNG demand is growing very quickly while inventories are at five years low. Moreover, we expect good rates supported by the high LNG prices on Asia. It opens the arbitrage and increases the tone-miles demand. In contrast, taking a look at the orderbook, we have 15-16 vessels without contract coming in 2021, much less in 2022 and none in 2023-2025. I guess this is the reason for the recent deals in the segment. Gaslog was taken private recently by BlackRock and Höegh LNG by Morgan Stanley. However, I don’t expect Golar shipping fleet being acquired by a PE because Golar fleet does not consist of modern vessels with long-term charters attached. Therefore, Golar has two feasible options, either merge the LNG segment with Gaslog Partners, which has a very similar fleet but just more TFDEs and Steams and a modestly better capital structure, or it can spin it off to the shareholders. In either scenario, I think they will be forced to offer cash/NFE shares to reduce the net debt to NAV. I expect Golar paying down anywhere from $100M to $200M and they can use between 2M and 4M NFE shares. In any case, Golar spinning the LNGC segment off in the next 18 months will unlock a lot of value due to non-sense current Golar stock price which implies the LNGC segment being worth $0 or negative, but if not, I expect the LNG shipping becoming a positive contributor, different from past years.

Source: Fearnleys

In summary, we are extremely confident the market is not valuing Golar's assets and fundamentals properly. Additionally, Golar is a disruptive and growth company lead by an excellent management. Even if the last three years have been a nightmare for Tor Olav Trøim, a big part of it was just bad luck, for instance, Hygo’s IPO failure. The new strategy focused on the FLNG segment seems did not fit with Iain Ross and he decided to exit Golar. Golar quickly appointed Mr. Karl Fredrik Staubo as the new Chief Executive Officer whose profile is better suited with the new strategy.

Before questioning Golar’s track record, you should know that they have built Hygo business from scratch and are booking gain of approximately $740M in only 5 years, they are the world’s first company to convert ships into FSRUs and FLNGs and harness waste energy to improve the efficiency of both. Always bear in mind that this is not a simple shipping company but an engineering company.

Recommended for you:

#136680

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Aquí que habláis de energéticas, este video es interesante: