Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Analyticss

En madrid, una familia que ingrese 3.000€ al mes netos entre los dos, despues de impuestos, y tenga 2 hijos, puede vivir perfectamente, y llevar a sus hijos a un buen colegio y universidad.

Pero claro, para hacer cosas caras pues como que no da,y para ahorrar barbaridades de dinero tampoco.

#114315

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Analyticss

Es verdad que ese dinero de la UE hubiese sido mejor aprovechado si se hubiese creado con ello buenas industrias porque las industrias generan trabajo en el lugar donde estan, pero España ha sido capaz de crear de las mejores empresas de infraestructuras del mundo, solo hay que ver a ACS de las mejores si no la mas grande en su sector, o Acciona, otra mas de lo mismo, ademas de Abertis en gestion, y constructuras como Sacyr y OHL y otras en su momento puntero como lo fue Abengoa o incluso una de las 3 mejores empresas de del mundo en aerogeneradores, como Gamesa, que compartia liderazgo con Vestas, donde el mapa mundial se dividia en siemens, en vestas gamesa y GE,y encima en el tramo de las petroleras y perforaciones, tenemos a tecnicas reunicas, una tambien lider en su sector o con muy buena posicion,y ya si me apuras Iberdrola, de las mas grandes del mundo entero, en su sector de redes y renovables.

Obviamente con el tiempo solo han ido quedando lideres unas pocas, como ACS y Acciona, pero en su dia eran punteras muchas de ellas.

Es verdad que las constructoras y empresas de infraestructuras solo crean trabajo alli donde construyen... por eso ha sido mal usado esos fondos, mejor haber creado industria que constructuras, pero que un pais como España, haya poseido un grupo de empresas de infraestructuras y constructoras lideres a nivel mundial, solo se ha podido hacer gracias a ese dinero de los fondos y a haber tirado el dinero en megalomanias en el pais.

pero es preferible tener Gamesas que no se dejen comprar, que accionas, acs o tecnicas reunidas que al final solo crean empleo alli donde esta la obra.

#114316

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

En los proyectos EPC que ejecutan las empresas de construcción, oil&gas, renovables, etc. también se genera empleo en la fase de ingeniería e incluso priorizan los suministradores españoles en la fase de aprovisionamiento.

Lo mismo ocurre con el sector naval o la automoción, que pueden llegar a mover mucho dinero en la economía de una país por ser un sectores muy especializados que generan a su vez una industria auxiliar muy potente. El claro ejemplo de esto es el sector offshore tanto en la industria naval como en el oil&gas en Noruega o el sector de la automoción en Alemania.

Potenciar cualquier industria que ejerce una posición dominante en una zona geográfica determinada puede llegar a generar unas sinergias impresionantes.

Nuestros líderes, lamentablemente, han priorizado crear una sociedad clientelar en España respecto a dominar cualquier sector económico y tecnológico a nivel mundial, y así nos va. Si Monturiol e Isaac Peral hubieran nacido en cualquier país al norte de los pirineos, ese país hubiera construido una industria tecnológica dominante a nivel mundial entorno al submarino, pero nacieron aquí, donde las prioridades son otras.

#114317

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Fun TradingMarketplaceBioFollowSpecial Situations, Contrarian, Long/Short Equity, ValueContributor Since 2013I am a former test & measurement doctor engineer (geodetic metrology). I was interested in quantum metrology for a while.I live mostly in Sweden with my loving wife.I have also managed an old and broad private family Portfolio successfully -- now officially retired but still active -- and trade personally a medium-size portfolio for over 40 years.“Logic will get you from A to B. Imagination will take you everywhere.” Einstein.Note: I am not a financial advisor. All articles are my honest opinion. It is your responsibility to conduct your own due diligence before investing or trading.Summary

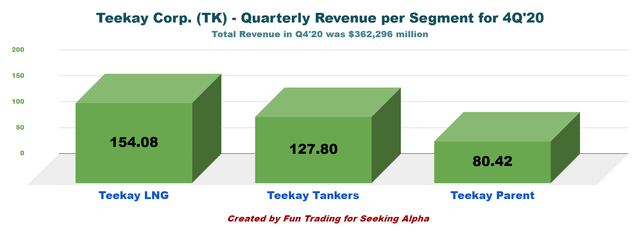

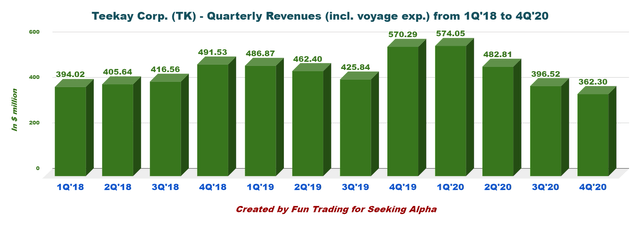

Operating consolidated revenues were $362,296 million in Q4, down 36.5% from the same quarter a year ago and down 9.4% sequentially.

Total adjusted EBITDA came to $221.062 million in the fourth quarter of 2020, down 38.2% over the same period of the prior year ($325.465 million).

The expected World recovery and the booming LNG sector give us reasons to be optimistic.

The investment thesis that I recommend is to start accumulating the stock with a long-term horizon. However, trading short-term about 30% of your long position is crucial.

Looking for a helping hand in the market? Members of The Gold And Oil Corner get exclusive ideas and guidance to navigate any climate. Learn More »

Source: Teekay Corp. Presentation

Investment Thesis

The Bermuda-based Teekay Corporation (NYSE: TK) released its fourth quarter of 2020 results on Feb. 25, 2021.

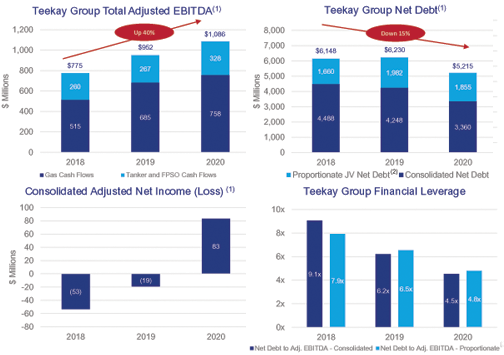

Q4 results were overall decent from Teekay Parent and Teekay LNG, while Teekay Tankers' results reflected the tanker market's recent weakness. For the full year 2020, the company reported consolidated adjusted net income of $83 million or $0.82 per share, compared to an adjusted net loss of $19 million or $0.19 per share in 2019.

Note: These results included the company’s two publicly-listed consolidated subsidiaries, Teekay LNG Partners L.P. (NYSE: TGP) and Teekay Tankers Ltd. (NYSE: TNK), collectively called the daughter Entities.

Both are trading on the NYSE, separately. However, Teekay, including its subsidiaries other than the daughter Entities indicated above, is referred to in this release as Teekay Parent.

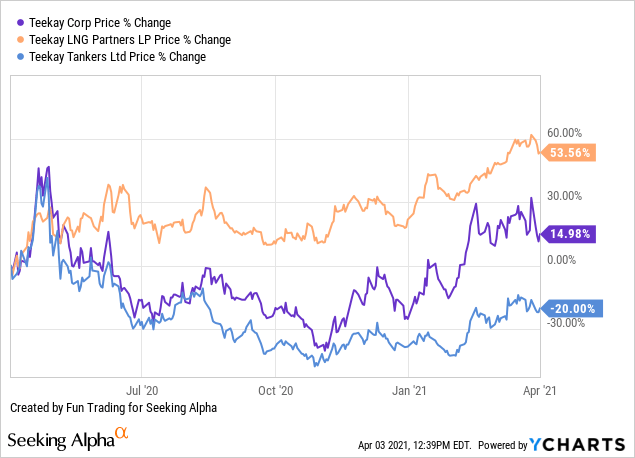

Hence, Teekay Corp represents an attractive and diversified way to participate in the potential appreciation in TGP and TNK, especially in H2 2021.

One important element is that the Teekay group has allocated most of its capital to the growing LNG segment over the past two decades. A quick look at TGP is showing the importance of this segment for the group.

CapEx for gas now represents about 80% of the total CapEx, and Tankers get the remaining ~20%.

The investment thesis that I recommend is to start accumulating the stock with a long-term horizon.

As I said in my preceding article, the world economy will probably recover by H2 2021 or sometime in 2022, at the latest, and companies like Teekay Corp. will necessarily benefit from that. The expected World recovery and the booming LNG sector give us reasons to be optimistic about this company's future.

However, the best strategy that I recommend is to trade short-term your long-term position. I think it is reasonable to allocate about 30% to 40% of your TK position for this purpose. It will provide you with an extra gain whereas reducing the risk of a severe unannounced downturn.

[I]t's been a very busy year. With record annual results at Teekay LNG and Teekay Tankers, we have strengthened our balance sheets and build resilient financial positions. We've also performed well from an operations and commercial perspective despite the challenges resulting from COVID-19, which we have so far successfully overcome.

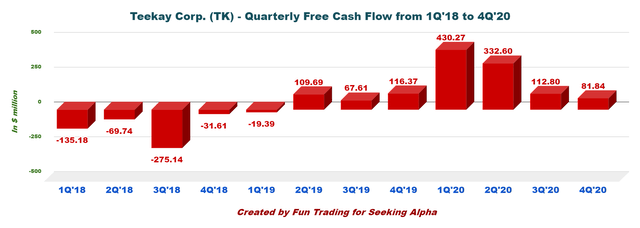

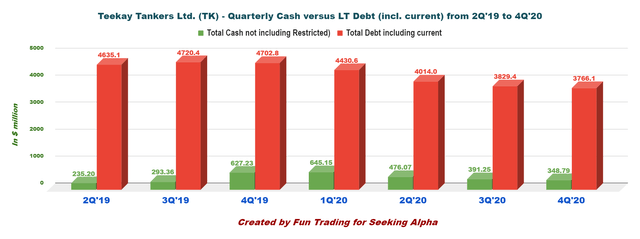

TK - The Raw Numbers: Fourth-Quarter Of 2020 And Financials History

TK Corp. (Consolidated) | 4Q'19 | 1Q'20 | 2Q'20 | 3Q'20 | 4Q'20 Total Revenues in $ Million | 570.29 | 574.05 | 482.81 | 396.52 | 362.30 Net Income in $ Million | 11.34 | -44.81 | 21.72 | -35.41 | -19.44 EBITDA $ Million | 275.01 | 191.23 | 230.51 | 79.84 | 85.17 Adjusted EBITDA in $ Million | 325.47 | 342.20 | 315.87 | 227.00 | 201.06 EPS diluted in $/share | 0.11 | -0.49 | 0.21 | -0.35 | -0.19 Operating cash flow in $ Million | 127.18 | 438.96 | 336.73 | 118.44 | 89.88 CapEx in $ Million | 10.81 | 8.69 | 4.14 | 5.64 | 8.04 Free Cash Flow in $ Million | 116.37 | 430.27 | 332.60 | 112.80 | 81.84 Total cash (not incl. Restricted) $ Million (three units) | 627.23 | 645.12 | 476.07 | 391.25 | 348.79 Long-term debt (incl. current) In $ Million | 4,702.84 | 4,430.62 | 4,014.02 | 3,829.43 | 3,766.1 Shares outstanding (Basic) in Million | 101.43 | 100.89 | 101.20 | 101.11 | 101.11Source:Teekay releaseAnalysis: Revenues, Earnings Details, Free Cash Flow1 - Operating Revenues (incl. Voyage expenses) were $362.30 million in 4Q'20Operating consolidated revenues were $362,296 million in Q4, down 36.5% from the same quarter a year ago and down 9.4% sequentially. The net loss attributable to shareholders of Teekay was $19.44 million, or $0.19 per share. The adjusted net income attributable to shareholders of Teekay was $2.8 million, or $0.03 per share.Total adjusted EBITDA came to $221.062 million in the fourth quarter of 2020, down 38.2% over the same period of the prior year ($325.465 million).The Company’s consolidated results during the fourth quarter of 2020 decreased compared to the same period of the prior year, primarily due to lower earnings from Teekay Tankers as a result of lower average spot tanker rates and a higher number of scheduled dry-dockings during the fourth quarter of 2020, as well as the cessation of production of the Petrojarl Banff (Banff) FPSO unit in June 2020 due to the decommissioning of the Banff oil field.Source: TK Presentation2 - Free cash flow is estimated at $81.84 million in 4Q'20Note: Free cash flow is cash from operations minus CapExTeekay Corp.'s 2020 free cash flow is $957.51 million with a Q4 consolidated free cash flow of $81.84 million.3 - Debt analysis: Net debt is estimated at $3.42 billion in 4Q'20 (consolidated and including current)Teekay Corp. reduced proportionate net debt by $560 million, or over 10% from the same quarter a year ago. Liquidity has increased to $1.0 billion this quarter. In the press release, the company said:

As at December 31, 2020, Teekay Parent had total liquidity of approximately $173.4 million (consisting of $44.8 million of cash and cash equivalents, and $128.6 million of undrawn capacity from a revolving credit facility). On a consolidated basis, as at December 31, 2020, Teekay had consolidated total liquidity of approximately $1.0 billion (consisting of $348.8 million of cash and cash equivalents and $658.8 million of undrawn capacity from its credit facilities).

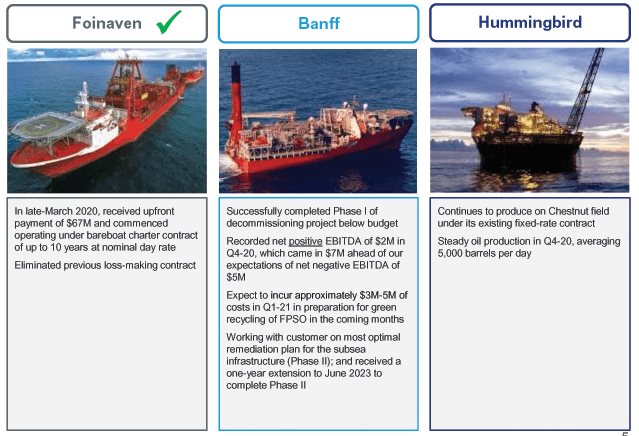

4 - Teekay's parent Winding down the FPSO segment.

It has been the company's weakest link, and many shareholders have been upset with how the company managed it. The decommissioning of the Petrojarl Banff FPSO remains a major negative on cash flows.

However, the company completed phase I of the decommissioning.

Source: TK Presentation

Teekay Parent's results improved due to the new Foinaven FPSO contract entered into March 2020, higher cash flows from the Hummingbird FPSO, and lower net G&A and interest expense partially offset lower earnings from the Banff FPSO, which ceased production and entered decommissioning in June 2020.

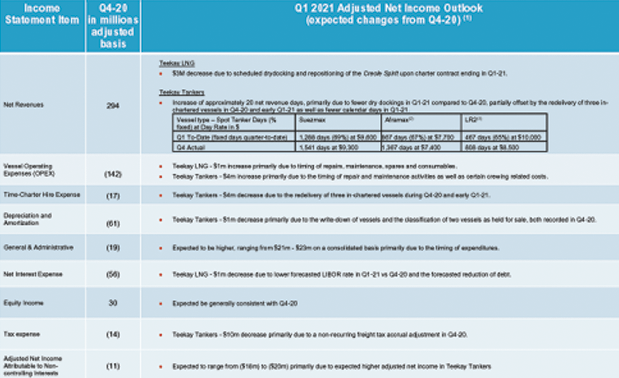

5 - Q1'2021 outlook

Source: TK Presentation

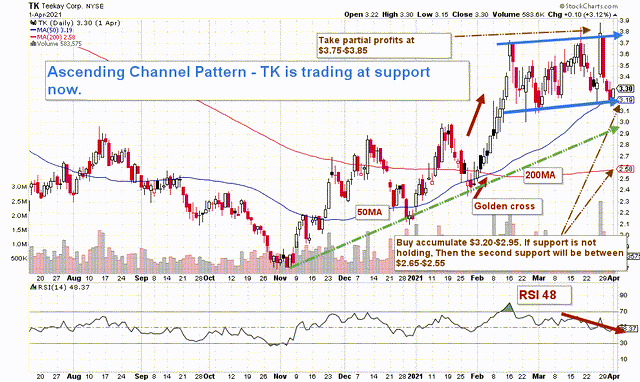

Technical Analysis (Short Term)

Teekay Corp. has wonderfully recovered from its November 2020 lows. The stock has more than doubled in the last six months, and it is normal to experience a temporary period of consolidation.

Its two daughter Entities (TPG and TNK) expect to do well in 2021, especially the LNG segment.

Technical Analysis

TK forms an ascending channel pattern with a line resistance of $3.75 and line support of $3.18.

The trading short-term strategy will be to sell partially (35%~) at resistance or a range of $3.75-$3.80 and buyback if the stock retraces to its pattern support at $3.15-$3.20. If TK crosses its pattern support (breakdown), I expect the stock to drop to its 200MA between $2.55-$2.65. Conversely, if TK momentum is strong, I expect the stock to reach the range of $4.60 -$5.40.

Author's note: If you find value in this article and would like to encourage such continued efforts, please click the "Like" button below as a vote of support. Thanks!

Join my "Gold and Oil Corner" today, and discuss ideas and strategies freely in my private chat room. Click here to subscribe now.

You will have access to 57+ stocks at your fingertips with my exclusive Fun Trading's stock tracker. Do not be alone and enjoy an honest exchange with a veteran trader with more than thirty years of experience.

"It's not only moving that creates new starting points. Sometimes all it takes is a subtle shift in perspective," Kristin Armstrong.

Fun Trading has been writing since 2014, and you will have total access to his 1,988 articles and counting.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: I trade short-term TK occasionally.

@LallemandI let you decide, I own TGP, and it is important to know that TGP is a part of TK and TNK that I will publish soon. I see some opportunity with a possible recovery down the road for TGP, TNK, and TK. I am just presenting the companies here. I recommend reading my article on TGP.

There are going to be a few disgruntle $TK longs reading this article myself included.. It was a major failed investment for me but now a trading stock with possible options strategies to recover some of my equity..

@rusty13 Same here. J. Mintzmyer pounded the table on TK a few years ago when it was near 10 (probably in 2018). Then TK became TKO. I don't have enough respect for TK to trade it, there are other stocks to trade.

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Analyticss

cierto, muchas fabricas de materiales para las infraestructuras españolas tambien han florecido al calor de las obras, el caso es de que España, no ha sido capaz de mantenerlo funcionando, despues de la crisis inmobiliaria, muchas de estas empresas se han ido al garete y por tanto ya era mas complicado encontrar proveedores españoles competentes para nuevas obras en el extranjero, al final una concesion de obra tiene unos pasos que seguir y debes ofrecer un buen precio, si España no tiene proveedores competentes, se prefiere los locales del pais.

Ess decir, podriamos haber creado buenos conglomerados de infraestructuras integradas, pero el modelo español no sabe funcionar y asi ha pasado.

pero ni mucho menos despreciable, ni hay que despreciar las empresas de infraestrcuturas y construccion y todo lo que ha nutrido por detras a estas empresas, ya que bien llevado hubiese sido una buena fuente de valor.

pero bueno, al final las maquinas con las que las empresas españolas conostruyen sus proyectos, o son alemanas, o son japonesas o son estado unidenses... siempre hay sectores mas integrados y de mejor calidad.

#114319

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

En los proyectos EPC que ejecutan las empresas de construcción, oil&gas, renovables, etc. también se genera empleo en la fase de ingeniería e incluso priorizan los suministradores españoles en la fase de aprovisionamiento.

Putas, sobornos y/o concursos trucados. En muchos casos es así de triste.

Investing is where you find a few great companies and then sit on your ass - C.M

#114320

Re: Cobas AM: Nueva Gestora de Francisco García Paramés