El peso de Munger es enorme, no me atrevo a tanto, aun así, voy a ir incrementando. Acabo de leer que Enrique Roca también las lleva.

Por otro lado hay tan pocas alternativas de inversión, que los índices no caen, solo hay rotación, según como vaya dándose el año, sobre todo con respecto a la evolución de la inflación (se comenta que quizás ya estemos en el pico), se parara la rotación y puede que volvamos a valores que lo han hecho bien los últimos años. Creo que tasas mayores de interés no tienen porque afectar a las grandes tech por poner un ejemplo.

#139123

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

I lay out the key issues that have been impacting BABA stock.

Recent crackdowns in the fintech and internet sector seemed to be favoring Alibaba Group.

The favorable media coverage of Charlie Munger's doubling-down of his BABA shareholding is a departure from his first two entries which received rather muted responses.

I rate BABA stock a 'buy'.

DNY59/E+ via Getty Images

Why Has Alibaba Stock Gone Down?

Alibaba Group (BABA) is one of the most followed stocks on Seeking Alpha but I shall not assume all who are reading this article are aware of what has bedeviled the Chinese internet titan over the past year. Hence, for the majority who are, by now, well-cognizant of the key issues, allow me to quickly help the uninitiated get up to speed.

In October 2020, BABA stock was riding high on the fervent investor anticipation of the pending public listing of its majority-owned unit. Unfortunately for shareholders, the IPO of Ant Group was suspended at the eleventh hour. Apparently, the regulators decided it was better for the market players to mistake them for being a party spoiler and out to wreck Jack Ma & Co. than let Ant Group become public before they could figure out how to regulate the fintech industry properly.

Frankly, the Chinese regulators would be condemned either way. If they had let Ant Group's IPO go through, it would be akin to DiDi Global's (DIDI) case. The latter ignored hints from the Chinese government to delay its IPO but DiDi bulldozed its way to a New York listing anyway.

Perhaps DiDi's executives thought that the regulators would be lenient to them once they are listed. After the bad press from the seemingly heavy-handed bringing down of Alibaba Group-Ant Group, maybe the regulators would be more conscious of the public perception? If this was indeed their thinking, the executives were very wrong. The Cyberspace Administration of China fired the first salvo, ordering app stores to remove DiDi's app. The rest, as the saying goes, is history.

Less than a month later, the world was reminded again of Beijing's resoluteness in carrying out what they had deemed to be necessary for the good of the population. Literally with a stroke of a pen, an entire industry - after-school tutoring - was condemned to be only non-profit organizations, a move that had "shocked even some of the most seasoned China watchers," as a Bloomberg commentary noted.

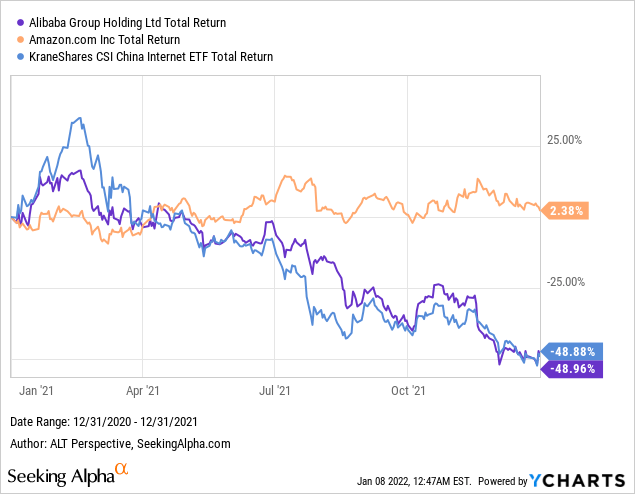

When investors think of Chinese stocks, Alibaba Group Holding comes to mind. Hence, fears about Chinese stocks, and in particular internet ones, extend to BABA. Even though the KraneShares CSI China Internet ETF (KWEB) has dozens of holdings, it fell by the same 49 percent as BABA in 2021. In the same period, Amazon.com, Inc. (AMZN) eked out a small gain of 2.4 percent.

Subsequently, although the worst fears did not materialize, the push for 'Common Prosperity' by Chinese President Xi Jinping led to fresh concerns over profitability as companies eagerly announced donations and programs in line with Beijing's policy directions. Alibaba pledged US$15.5 billion and despite evidence to the contrary that the 'spending' wouldn't 'go down the drain', jaded shareholders decided to bail out.

Remaining longs and a fresh batch of bargain hunters (or daredevils?) had to endure reignited fears over the delisting of Chinese ADRs as well as an unsubstantiated Bloomberg report on a VIE ban that surfaced in early December.

The above-mentioned jitters were sparked mostly by a lack of understanding or misinterpretations over Beijing's intentions. The delisting threat posed by the Holding Foreign Companies Accountable Act (HFCAA) of the U.S. added another layer of uncertainty.

To make matters worse, I argued in Alibaba: 'New' Risk Was Hiding In Plain Sight that the Biden administration could be expanding an investment ban on Chinese internet stocks like Alibaba Group Holding. If this risk materializes, Americans would not even be able to own the Hong Kong shares of Alibaba. The ensuing sell-off to comply with the supposed executive order could be uglier than anything we had seen in 2021.

Is Alibaba Stock Expected To Rebound?

I attempted to answer this popular question several times last year and each time it made me look like a fool only a few days later, like this in May and this in October. If BABA stock had rebounded and subsequently returned the recovery gains, that would still be a consolation. However, BABA went further south after each rebound attempt. In other words, it was establishing lower highs and lower lows.

After a turbulent 2021, Alibaba's share price has been fairly resilient in the new year. On the contrary, high-growth, profit-lacking stocks have taken a beating in the past weeks. What had initially seemed to be an unjustified weakness attributed to year-end tax-loss selling worsened due to escalating concerns over interest rate hikes making such stocks less attractive.

As I own some of these stocks like Teladoc Health (TDOC) and Coupa Software (COUP), it was like reliving the experience of owning BABA all over again. Each time I reviewed their fundamentals and concluded it made better sense to hold, these stocks headed south anyway.

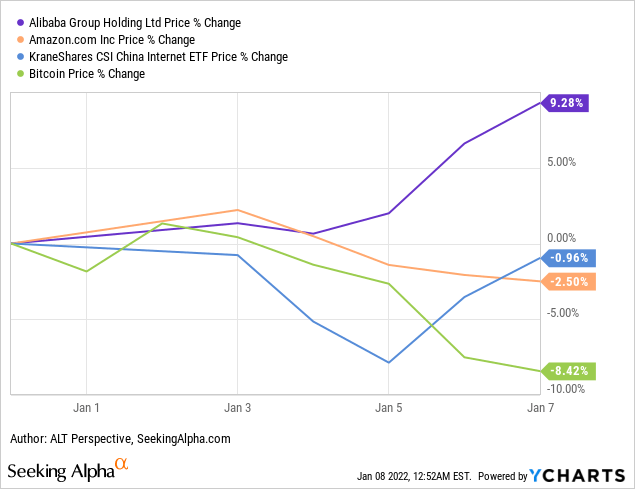

Nonetheless, for the first few days of the year at least, BABA shareholders have been enjoying the rare relief, with the stock up 9.3 percent thus far. In the comment section where it's common to encounter the saying "I would rather own cryptocurrencies than BABA," I am ashamed to say I felt moments of schadenfreude knowing that the price of Bitcoin (BTC-USD) is down 8.4 percent. Less well-known cryptocurrencies like Dogecoin (DOGE-USD) and Shiba Inu (SHIB-USD) have seen worse losses.

Of course, we have seen this movie many times. However, at the risk of sounding like a broken clock, I think this bullish start to 2022 can continue. I explained in a recent article Which Are The Best Chinese Stocks To Watch In 2022? why I believe Beijing is not reversing its policy and going on a campaign to nationalize private entities as some critics charged.

I also noted in the article that investment experts are seeing signs of the heavy-handed crackdown ameliorating in 2022. For instance, Thomas Poullaouec, head of Asia-Pacific multi-asset solutions at T. Rowe Price, said in a note to clients that Beijing has "hinted it would go easier on regulating big private sector players" and that "excessive capital growth may instead be curbed through other mechanisms."

Following that article, I encountered a SA news article saying that Wedbush analyst Dan Ives believes the Chinese government will continue to crack down on companies, keeping their share prices depressed and resulting in more funds shifting from Chinese tech stocks and rotating into U.S. tech stocks. Ironically, from what we have seen in the past few days, the reverse appears to be happening.

Shareholders of BABA should perhaps thank a key English publication typically employed by the Chinese Communist Party to communicate its message for the global audience. A recent op-ed from the Global Times had ostensibly played a major role in boosting the bullish sentiment.

While the article is rather balanced and raises the woes and challenges facing Alibaba Group, some parts read like a paid write-up by the company. The following paragraph is an example (emphasis mine):

"Over the coming months, Alibaba group will pursue a more segmented shift, moving from a super-app strategy to a multi-app entry strategy, which is expected to assist the company to better respond to market competition. And, Alibaba should be able to strengthen its core e-commerce business in tier-one and tier-two Chinese cities by tapping into its technological advantages in AI and big data insights."

Wen Sheng, the author of the article and an editor with the Global Times, went on to praise Alibaba's announced initiatives, saying those would "align the company more closely with Chinese government's policy priority, which is obviously a wise move." He even titled the article Alibaba likely to emerge from 'dark woods' in 2022.

Alibaba Group had previously gone on a shopping spree of media assets such as social media platform Weibo (WB) and news outlet South China Morning Post. With the state media speaking in the positive of Alibaba, why would it need them anymore?

Indeed, Alibaba had reportedly discussed a sale of its 30 percent stake in Weibo to a state-owned media company. This could mark the beginning of its divestment phase. Shedding non-core assets would make Alibaba less of a regulatory target and enable the company to redeploy the funds for more productive purposes.

I'm a nobody, especially compared to Cathie Wood who conceptualized the ETFs of Ark Invest. Thus, while she can convince investors to have a "five-year investment time horizon" to potentially enjoy "a 30-40% compound annual rate of return during the next five years," I will simply continue discussing developments related to Alibaba Group, without venturing into the business of providing fanciful projections.

Recent Crackdowns in the Fintech and Internet Sector Seemed to Favor Alibaba Group

When the IPO of Ant Group was abruptly suspended, the dominant narrative was that the Chinese government was out to 'fix' Jack Ma, the founder of Alibaba Group and Ant Group. Beijing was 'suddenly' cracking down on the wild world of the fintech industry.

However, way back in 2015 when Ant Group was still known as Ant Financial Services Group, China's central bank had already censured the company over some of the promotional tactics it employed. As the fintech giant expanded, there were numerous other brushes with the authorities.

Nevertheless, the regulators have been transparent and those penalized aren't necessarily related to Alibaba Group. The latter may even be a beneficiary in certain regulatory actions. For instance, China's central bank slashed the number of licenses to operate third-party payment services by more than 20 percent last year. Ant Group can potentially expand its market share with the exit of these terminated players.

The benefits to Alibaba Group from the opening of the walled garden of WeChat, the super-app operated by Tencent Holdings (OTCPK:TCEHY)(OTCPK:TCTZF), have been discussed before. However, the true 'empire' of Tencent goes beyond its own platforms and its ongoing drive to play by the regulators' books continues to strengthen Alibaba.

Perhaps cognizant of its heft from its myriad savvy investments, Tencent has been making a series of divestments ostensibly to make itself appear 'smaller' and less of a regulatory target. Recently, Tencent announced that it will distribute the bulk of its shareholding of JD.com (JD) to shareholders. From owning 17.0 percent of JD, Tencent would hold only around 2.3 percent of the largest retailer in China.

Although JD and Tencent declared the duo "will continue to maintain their mutually beneficial business relationship, including their ongoing strategic partnership agreement," it is only reasonable to expect a step-back in cooperation following the divestment exercise.

Tencent also has a substantial stake in Pinduoduo (PDD), whose share price has slumped following speculations that it could be one of the next few holdings in line for divestment. JD and PDD are the two e-commerce giants challenging Alibaba for dominance in the sector. The reduced involvement of their key backer, Tencent, could weaken their competitive edge against Alibaba's e-commerce platforms.

A possible 'standalone' Meituan (MEIT)(OTCPK:MPNGY)(OTCPK:MPNGF), which also counts Tencent as a key shareholder, may also be taken advantage of by Alibaba's lifestyle service offering, Alibaba Local Services Co. The division houses travel-services platform Fliggy and mapping and navigation app Amap under one roof, including on-demand delivery app Ele.me and local commerce platform Koubei.

At the same time, Tencent is also engaging itself with legal battles against ByteDance (BDNCE) over copyright infringement. The latter has increasingly been encroaching on the traditional turfs of both Tencent and Alibaba. With both mega rivals of Alibaba, Tencent and TikTok owner ByteDance occupied with legal attacks against each other, Alibaba could enjoy a moment of relief to focus on growing its businesses.

Alibaba Stock Key Metrics

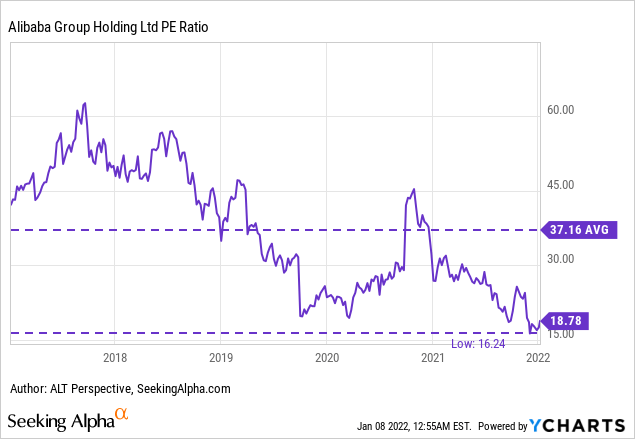

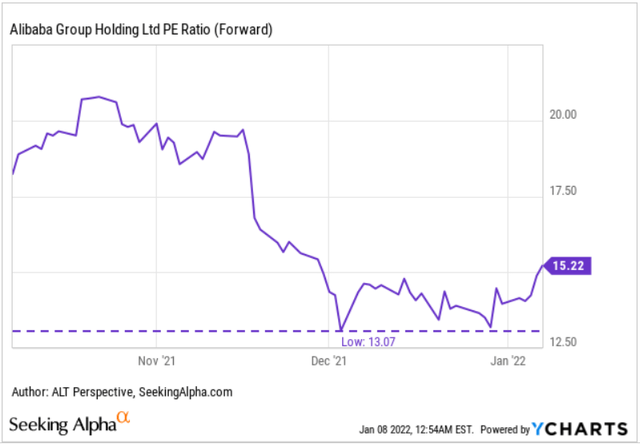

While discussing a stock on the investment site Seeking Alpha, we cannot avoid looking at some key metrics. For BABA, there is no need to hide as the financial numbers and ratios are very attractive. For instance, its price-to-earnings ratio is a mere 18.8 times currently, up from a recent low of 16.2 times but around half that of the five-year average at 37.2 times.

Amid its 'common prosperity' commitments, penalties, and business adjustments in response to the tighter regulatory environment, analysts are still expecting Alibaba Group to report higher profitability this year. Hence, the P/E ratio on a forward basis is even lower at 15.2 times.

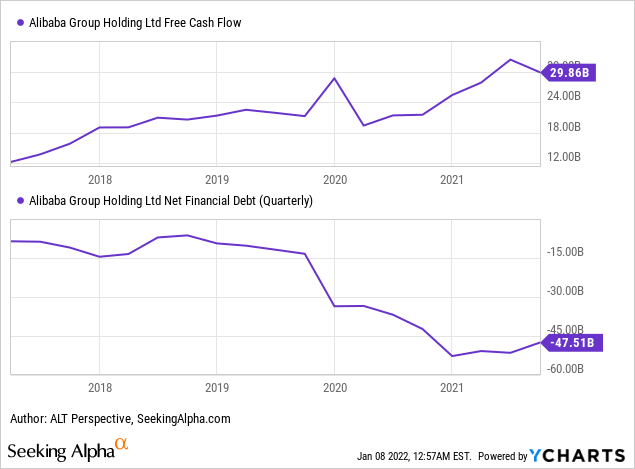

All this while, Alibaba Group's free cash flow continues to be on a multi-year uptrend. That has helped the e-commerce and cloud giant to grow its net cash, which has climbed to $47.5 billion by the third quarter of 2021.

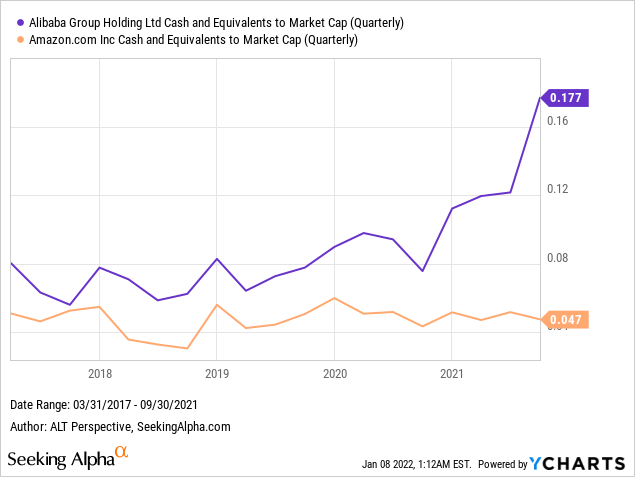

To put Alibaba's cash position in perspective, I generated the following chart comparing Alibaba's cash and equivalents to its market cap and contrasted that with Amazon. Alibaba has long demonstrated its superiority over Amazon on cash and equivalent to market cap. The disparity widened sharply in the third quarter of 2021.

Is BABA Stock A Buy, Sell, Or Hold?

Even though BABA stock is trading at a more than four-year low, its financial position continues to strengthen. As pointed out earlier, Alibaba's business growth prospects look optimistic with the current regulatory crackdown impacting its rivals negatively.

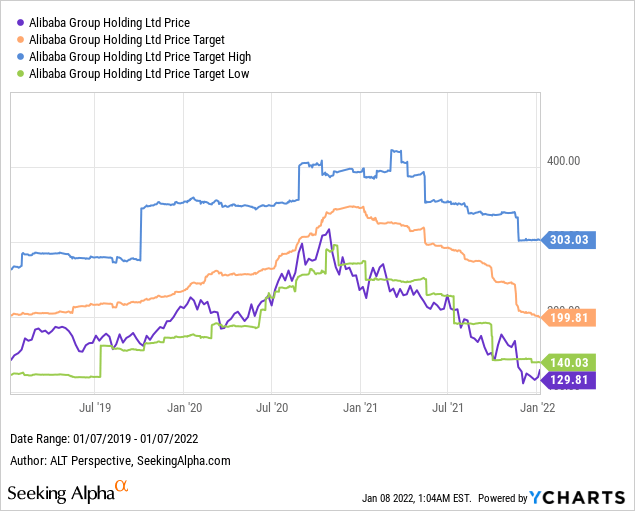

A series of downgrades have sent the consensus price target of BABA back to where it began three years ago. BABA stock's relative resilience since the beginning of the year will help analysts tell a story of improved sentiment and should make them confident of raising the earnings forecasts of Alibaba and consequently its target price.

The favorable media coverage of Charlie Munger's doubling-down of his BABA shareholding in the fourth quarter of 2021 is a departure from his first two entries which received rather muted responses and some critics even charged he did so because he had lost his marbles or to score political points with Beijing. This has helped support sentiment. All above considered, I find BABA stock a 'Buy'. The share price has seemingly reached a floor in December when the stock suffered from a serious bout of tax-loss selling.

I am honored to have been categorized as a 5-Star financial expert and ranked among the top 2% of financial bloggers on TipRanks in 2017/18. For a period, I was among the top 3 “Opinion Leaders” for Insider Ownership and Services, as well as top 5 for Long Ideas and Fund Holdings. I am an avid reader of market news and company publications with the aim of improving my investment acumen. I enjoy expressing my findings and opinions through writings. My appreciation and understanding of business strategies improved to a whole new level since completing an MBA (Distinction) from a FT100 MBA school. I have worked in companies with businesses that span multiple industries, according me with the exposure to a myriad of sectors.Check out my Author's Picks and over 190 Editor's Picks, among the highest in Seeking Alpha, if not the most.

Show more

Show MoreFollow

Disclosure: I/we have a beneficial long position in the shares of BABA, JD, TCEHY, TDOC, COUP either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

LikeSaveShareCommentRecommended For YouComments (116)NewestPublishAasantana86Today, 12:26 AMPremiumMarketplaceComments (34)I know nothing, less than nothing, BUT since fundamentals apparently don't matter wiht this stock anymore - how about the the voodoo TA analysis which this stock has double bottomed at the .768 retracement dating back to it's multi-year takoff point on 10/2/2015. It's uncanny. Hard to call bottoms, but man does that look promisingReplyLikeKkarondongotbannedYesterday, 4:54 PMComments (3.13K)Stock price does not reflect a company. At the end of the day, BABA is a profitable company, thats whats important. And the stock price will tank to a point where its attractive enough to buy. Its all about price vs risk. I would say there is still room for BABA to drop, maybe ~100 - 110. then itll become attractiveReplyLikeJJason TorquitasToday, 1:08 AMComments (5)@karondongotbanned it did hit 108 earlier. Could it retest around there? Possible. It could also never look back and recover to 180-200 zone this yr.ReplyLike(1)KkevinconnollyYesterday, 4:51 PMComments (2.03K)Senior ALT, the usual high standards. When you have a minute or so check on Atimes. com ------Article January 11th, 2022 by David P. Goldman "Study forecasts China investment of $$$75 trillion in carbon neutrality." On David Goldman------the dude has been on point from the jump when it comes to the Middle Kingdom!! CIAO BELLA, Senior ALTReplyLike(1)ALT PerspectiveYesterday, 8:43 PMContributorPremiumComments (5.35K)@kevinconnolly Good read. When forecasts say China will spend $75T, everyone takes it for granted. Meanwhile, Congress is trying pass the $1.75T BBB bill.Reply

#139126

Re: Cobas AM: Nueva Gestora de Francisco García Paramés