Several factors suggest that the stock is ready to start heading in the right direction.

Alibaba's stock is remarkably cheap now at 10-12 times forward EPS estimates.

Charlie Munger just doubled down on Alibaba, and I followed his example.

I believe Alibaba's stock can move considerably higher from here, and shares may represent the deal of the decade right now.

This idea was discussed in more depth with members of my private investing community, The Financial Prophet. Learn More »

Andrew Braun/iStock Editorial via Getty Images

I don't typically follow Charlie Munger, but I double my stake in Alibaba (BABA) when I do. I began investing in Alibaba in 2015 around the $70-$85 region. The investment was going great for a while, but everything went south in late 2020. Alibaba topped out at about $320, and a perfect storm of harmful elements has plagued the company's share price ever since.

The company's stock recently hit a new multi-year low at around $110. This staggering decline represents a 65% drop, a remarkable downfall for one of the world's most dominant e-commerce giants. Alibaba's stock price was essentially reset to early 2017 levels, back when Alibaba produced one-fifth of its current revenues and had earnings fewer than one-third of what it has now.

Alibaba now trades at a rock-bottom 13.5 times 2022's consensus EPS estimates, while the company should continue to provide double-digit revenue growth and deliver substantial EPS expansion in future years. Moreover, the ongoing fears over delisting concerns, Chinese Communist Party ("CCP") intervention, and other variables seem overblown and are likely transitory. Therefore, the company's shares are on sale right now, should not remain depressed for long, and have a high probability of moving considerably higher as the company advances.

Why The Stock May Have Finally Bottomed

In addition to solid technical support at the $110-100 level and an exceptionally cheap valuation, one of Wall Street's most prominent value investors, Charlie Munger, is doubling down on Alibaba. The accomplished investor recently increased his Alibaba stake by 300,000 shares to roughly $78 million by today's market value. Moreover, other investors are turning bullish, citing lockdowns and other factors as possible catalysts for future gains in the company's share price. The phase of maximum pessimism concerning Alibaba may have passed, projections have been lowered considerably, and the company's stock price cascaded to levels not seen in years. Now the stock is stabilizing, analysts' forecasts should improve, and the company's shares could appreciate substantially in future years.

More Lockdowns Should Lead To More Profits

It's not that Alibaba needs China to implement more lockdowns. Nevertheless, it should benefit from the lockdown effect. Due to the continued spread of the coronavirus, the CCP recently locked down another million plus metropolis, Yuzhou. This lockdown came after Xi'an's 13 million populous got shuttered in on Dec. 23. Now, when China says lockdown, the government means it. Yuzhou's transport system is reportedly shut down, and only essential food stores remain open overnight.

Remember, China is hosting the Winter Olympics this year, and the country will likely continue implementing strict lockdown measures to build confidence and ensure safety leading into this momentous event. Many people in China already shop online, and I mean close to a billion by many. Increased lockdowns should push more buyers to purchase from Alibaba's online businesses.

With a reported 953 million AACs in China, it seems that just about everyone who shops online in the country have probably purchased something from an Alibaba-owned business. That's because Alibaba has amassed a monopoly over the years essentially. Sure, the company has competitors like JD.com (JD) and Pinduoduo (PDD), but Alibaba should remain the dominant player in China's online world.

Moreover, it's not just China. Alibaba is expanding, and the company now has more than 285 million international AACs. Combined, the company has around 1.25 billion global customers, and it's likely to experience more growth in the future. While the Chinese market is becoming more saturated, average consumer buying volume should continue to drive revenues higher in future years. Additionally, there's plenty of growth overseas for China's online giant.

We see that revenues increased by a very healthy margin last quarter. Total revenues jumped by 29%, while the company's core China commerce business revenues surged by 30% YoY. Even if we exclude the Sun Art acquisition, revenues expanded by about 15% YoY. International sales expanded by 34%, and cloud grew by 33% YoY. Therefore, we see very healthy growth in Alibaba's businesses. Moreover, increased lockdowns should help drive online traffic, and Alibaba can probably surpass the recently lowered and depressed consensus estimate figures.

We see that Alibaba missed earnings twice in the last three years. Both misses arrived recently, along with Alibaba's perfect storm of negative news flow and transitory fundamental developments. Nevertheless, lower EPS revisions continue to come in month after month.

Alibaba's revised EPS estimates are substantially lower than six, three, and even one month ago. However, before Alibaba's issues arose about a year ago, the company beat consensus estimates by an extensive margin. For instance, in 2019 and 2020, Alibaba beat consensus EPS forecasts by an average of approximately 20%-25%. Provided that the company's fundamental issues can prove transitory, Alibaba should return to its trend of surpassing analyst estimates. Moreover, due to the sharp revisions lower in earnings expectations, Alibaba may begin to exceed estimates substantially soon. Upward earnings revisions could follow, reflecting very positively on Alibaba's stock.

After the considerable revisions, consensus figures point to an EPS of $10.87 in 2023. Still, this estimate illustrates that Alibaba is trading at only 12 times forward earnings expectations now. Moreover, Alibaba may return to its trend of beating the consensus figures in 2023 and earn around $13 (20% more than expected). In such a scenario, the stock is only at ten times forward earnings now. Twelve times forward earnings is a cheap valuation. Still, 10 times is remarkably inexpensive, especially for a dominant market-leading company that should deliver double-digit revenue growth for years moving forward.

Much like EPS estimates, revenue estimates also have been brought down substantially over the last year. Nevertheless, we still see significant growth projections moving forward. We see a healthy revenue growth trajectory of around 17%-15% in 2022 and 2023, likely slowing down through 2025 and future years. Considering the healthy growth rate, and its valuation of 10-12 times lowered earnings estimates, Alibaba may be the deal of the decade right now.

What Alibaba's financials could look like moving forward from here:

I'm using slightly more bullish EPS estimates than in my previous article. However, I'm doing this because I believe the company can achieve my estimates and I also feel that my last report was too conservative. We see that by applying slight multiple expansion (that should occur once the negative risk factors get alleviated), Alibaba's stock price will likely move substantially higher with mild to moderate EPS growth. I also believe that current risk factors are vastly overblown and help provide a considerable investment opportunity. Therefore, I followed Charlie Munger's move and doubled down on my Alibaba position.

Will Alibaba Be Broken Up?

Sometimes I hear criticism that Alibaba's retail business may break up because it resembles a monopoly. However, the company has competitors in China. Moreover, I don't believe that China's regulators would have approved the $3.6 billion Sun Art acquisition if severe concerns about a possible breakup existed.

Will Alibaba Get Delisted?

I believe that the delisting concerns are greatly exaggerated. Moreover, China's regulatory agency recently stated that they respect where Chinese companies list shares. It also said that reports of a push for VIEs to drop their U.S. listings are a complete misreading and misrepresentation of the facts.

The SEC could potentially force Chinese companies to delist for failing to comply with accounting regulations, but only after three full years of non-compliance. Therefore, a hypothetical Alibaba delisting would not occur until 2024 in this scenario. Also, who says that Alibaba won't comply with the SEC's accounting requests? Moreover, Chinese companies and China's regulators cooperate with U.S. regulators to avoid any prominent delistings in future years.

Nevertheless, Risks Exist

While I'm bullish on Alibaba, various factors could occur that may derail my expectations for the company. For instance, the CCP could clamp down further on Alibaba and other Chinese tech giants. Moreover, U.S. regulators could decide to delist the company's ADRs. Increased competition could impact Alibaba's growth and profits. The company's growth could be worse than my current anticipation. Also, Alibaba's profitability could continue to struggle for various reasons. There are multiple risks to this investment, which is why shares are very cheap right now. In my view, Alibaba remains an elevated risk/high reward investment, and investors should carefully examine the risks before opening a position in Alibaba stock.

Note: Please consider, if anyone is concerned about delisting, you can buy Alibaba shares on the Hong Kong Exchange. I don't believe there is a substantial risk of delisting there.

Are You Getting The Returns You Want?

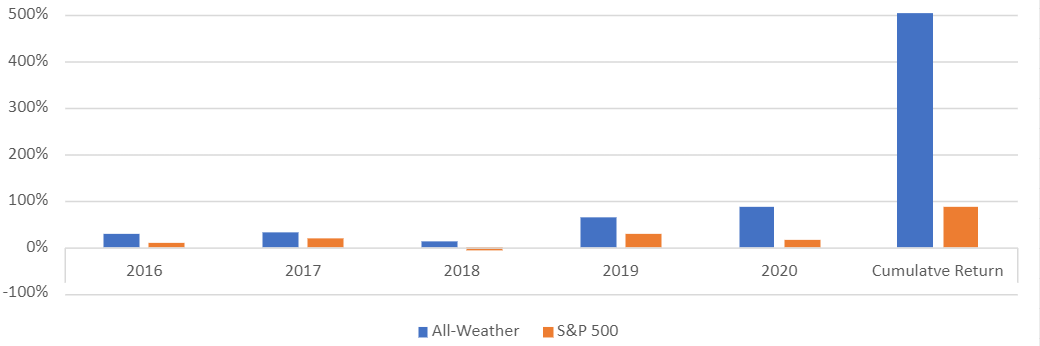

Invest alongside the Financial Prophet'sAll-Weather Portfolio (2020 return 87%), and achieve optimal results in any market.

Our Daily Prophet Report provides the crucial information you need before the opening bell rings each morning.

Implement our Covered Call Dividend Plan and earn an extra 40-60% on some of your investments.

All-Weather Portfolio vs. The S&P 500

Don't Wait,Unlock Your Own Financial Prophet!

Take advantage of the 2-week free trial and receive this limited-time 20% discount with your subscription. Sign up now, and start beating the market for less than $1 a day!

Hi, I am Victor Dergunov, MBA. Over the years, some of my top investments include Apple, Tesla, Amazon, Netflix, Facebook, Google, Microsoft, Nike, JPMorgan, Bitcoin, and much more. It all goes back to looking at stock quotes in the old Wall St. Journal newspaper when I was 16. What do these numbers mean, I thought, and more importantly, how do I make money from this? Fortunately, my uncle was a successful commodities trader on the NYMEX in the 70s and 80s, and I got him to teach me how to trade and invest. I bought my first actual stock in a company when I was 20, and the rest, as they say, is history.

Show more

Show MoreFollow

Disclosure: I/we have a beneficial long position in the shares of BABA either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.