We ended 2020 with strong Q4 performance as the business delivered substantial MAU growth, subscriber additions that exceeded our guidance, an improvement in ARPU trends, acceleration of users who engage with podcast content, better than expected Gross Margin, and Free Cash Flow of €74 million. Headwinds included the negative effects from FX movements, which were more severe than forecast and impacted revenue growth by 690 bps. Given the strong Q4 performance, we believe we are well positioned for continued growth in 2021.

MONTHLY ACTIVE USERS (“MAUs”)

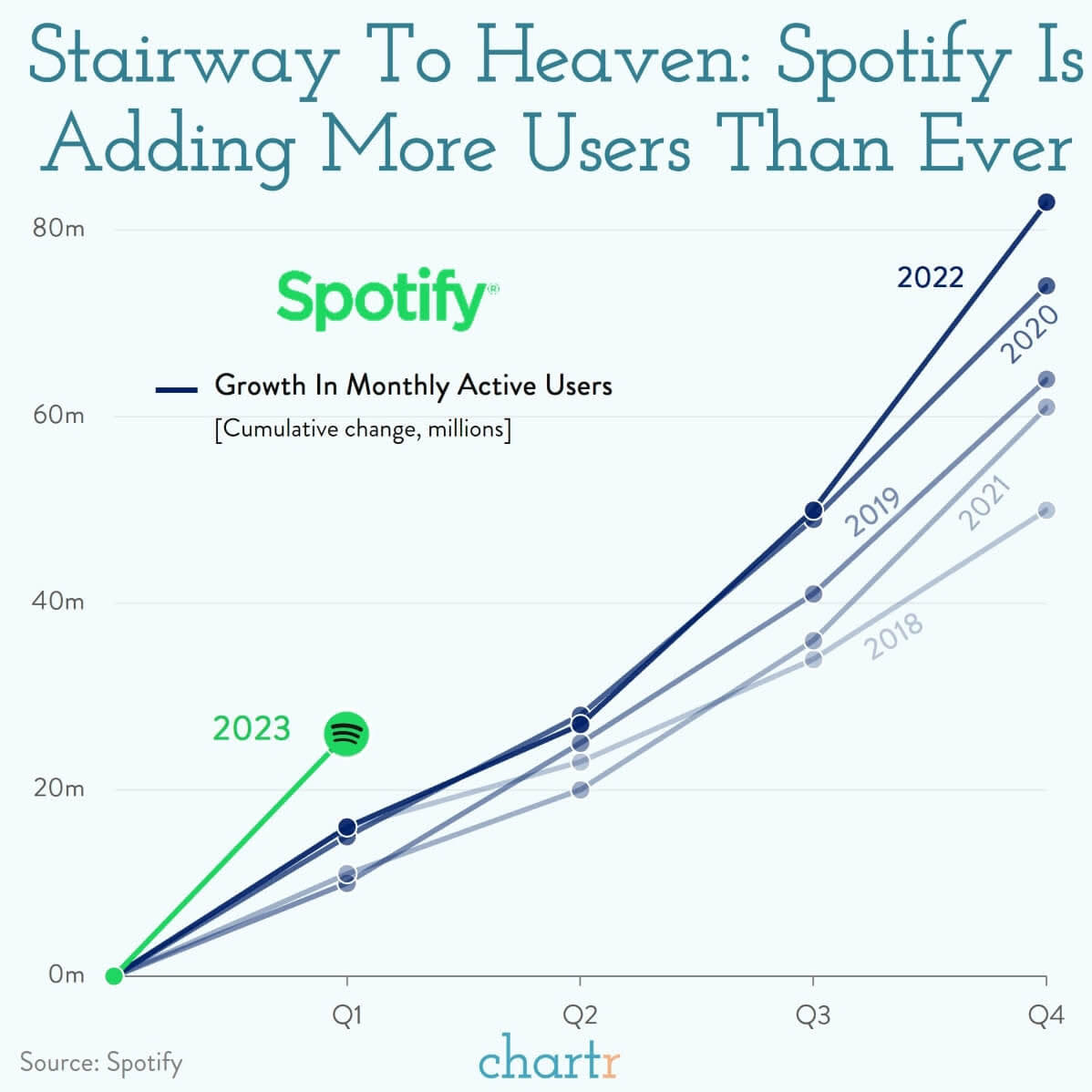

Total MAUs grew 27% Y/Y to 345 million in the quarter, reaching the top end of our guidance range. We continued to see healthy double digit Y/Y growth across all regions. For the full year, net additions accelerated to a record 74 million compared to 2019 net additions of 64 million. In Q4, we added 25 million MAUs and benefited from faster growth in India, US, and Western Europe, with India serving as a notable source of upside vs. our forecast driven by successful marketing campaigns. Based on the behavior we see when users first join Spotify, we are confident that podcast usage has been a factor in the accelerated net additions.

On December 2, 2020, we launched the 6th annual year-end Spotify Wrapped campaign. This year focused on engaging new audiences by demonstrating the power of listening to connect, celebrating and supporting our creator communities in a meaningful way, and evolving Wrapped to deliver a more purposeful and personal experience for our users. Within the first 24 hours of launch, the campaign exceeded the total engagement numbers for all of 2019. In total, more than 90 million users engaged with Wrapped content this year (vs. more than 60 million last year). This spurred more than 50 million shares of Wrapped stories and cards and a considerable amount of platform consumption on our three personalized playlists, with the latter driving 8% of total consumption hours on December 3, the day after launch.

Global consumption hours were up meaningfully in Q4 on a Y/Y basis. We have seen per user consumption in large regions such as Europe and North America return to growth, while Latin America and Rest of World show signs of improvement but remain slightly below pre-COVID levels.

PREMIUM SUBSCRIBERS

Our Premium Subscribers grew 24% Y/Y to 155 million in the quarter, exceeding the top end of our guidance range. For the full year, net additions accelerated to a record 30 million compared to 2019 net additions of 28 million. In Q4, we added 10 million subscribers, with all regions contributing to growth, led by Europe and North America. Europe continues to benefit from our July launch in Russia and 12 surrounding markets. Relative to our forecast, Latin America and Europe performed particularly well from a regional perspective, while Family Plan and Duo additions were strong from a product perspective.

Of note this quarter was the launch of Spotify Premium Mini in India and Indonesia, which gives users daily and weekly access to a subset of their favorite Premium features for a lower price as part of Spotify’s commitment to continuously explore new ways to improve our Premium experience. In Q4, we also announced partnership deals with Grab (Southeast Asia), Flipkart (India), Tink (Germany), and Euronics (Europe). On February 1, we announced that Spotify is now officially available in South Korea, the world's 6th largest music market.

Our average monthly Premium churn rate for the quarter was down slightly Y/Y and up modestly Q/Q. This was in line with expectations with the sequential increase due to churn from promotional plans. We expect churn to continue to decline in 2021.

FINANCIAL METRICS

Revenue

Total revenue of €2,168 million grew 17% Y/Y in Q4 or 24% Y/Y on a constant currency basis. Reported revenue was slightly above the midpoint of our guidance range, as FX headwinds of 690 bps were higher than the 600 bps incorporated into our plan. Excluding these headwinds we were slightly above plan. The depreciation of the US Dollar vs. the Euro was the primary driver of this variance. Premium revenue grew 15% Y/Y to €1,887 million (or 22% Y/Y in constant currency terms) while Ad-Supported revenue was particularly strong, growing 29% Y/Y (or 39% Y/Y in constant currency terms).

Within Premium, average revenue per user (“ARPU”) of €4.26 in Q4 was down 8% Y/Y (but down only 3% Y/Y in constant currency terms vs. down 6% Y/Y in Q3). Excluding FX, product mix accounted for the majority of the ARPU decline, followed by geographic mix, but was partially offset by reduced promotional activity. In October, we raised the price of the Family Plan in 7 markets (Australia, Belgium, Switzerland, Bolivia, Peru, Ecuador, and Colombia) alongside Duo in Colombia. Early results of the price increases have been highly encouraging, as we have seen no meaningful impacts to churn or customer intake in these markets. On February 1, we announced Family Plan price increases across an additional 25 markets (8 in Latin America, 12 in Europe, 4 in Rest of World and Canada in North America), including full portfolio price increases in Sweden, Norway, Finland, and Iceland. We expect continued sequential improvement in the Y/Y change in Premium ARPU in 2021 on a constant currency basis.

Ad-Supported revenue of €281 million outperformed our forecast. We saw strong Y/Y revenue growth across all of our regions and channels as advertiser demand continued to rebound from Q2 2020 lows. The strength in Ad-Supported revenue was led by our Podcast, Direct, and Ad Studio channels, with Podcast and Ad Studio both growing over 100% on a Y/Y basis. Podcast performance benefited from strong underlying demand from advertisers with a 50% increase in the number of companies spending in this channel vs. Q3. We saw healthy double digit CPM gains, along with contributions from The Ringer, The Joe Rogan Experience, and the acquisition of Megaphone (closed on December 8th). Streaming Ad Insertion (“SAI”), our targeted, impression-based podcast ad product, is now live across most of our Owned & Exclusive (“O&E”) portfolio and available in four markets (US, Canada, UK and Germany). Our Programmatic and Direct channels increased 12% and 7% Y/Y, respectively, due to a significant increase in impressions sold.

Gross Margin

Gross Margin finished at 26.5% in Q4, above the top end of our guidance range. Our Gross Margin expanded nearly 100 bps Y/Y, as Other Cost of Revenue efficiencies (e.g. payment fees, streaming delivery costs), a favorable revenue mix shift towards podcasts, and a change in estimated music royalties were partially offset by higher non-music and other content costs.

Premium Gross Margin was 28.9% in Q4, up from 27.3% in Q3 and up 145 bps Y/Y. Ad-Supported Gross Margin was 10.8% in Q4, up from 0.6% in Q3 and down 84 bps Y/Y. As a reminder, we now account for all content costs related to podcast investment in the Ad-Supported business.

Operating Expenses / Income (Loss)

Operating Expenses totaled €644 million in Q4, an increase of 17% Y/Y and above our plan. Higher than forecast Social Charges accounted for the overage given the increase in our share price during the quarter. Total Social Charges were €65 million, approximately €56 million higher than forecast. Excluding the impact of our share price volatility, Operating Expenses grew less than forecast at 7% Y/Y. Additionally, certain marketing expenses came in lower than expected due to campaign timing shifts and movements in FX.

As a reminder, Social Charges are payroll taxes associated with employee salaries and benefits, including share-based compensation. We are subject to social taxes in several countries in which we operate, although Sweden accounts for the bulk of the social costs. We don’t forecast stock price changes in our guidance so upward or downward movements will impact our reported operating expenses.

At the end of Q4, our workforce consisted of 6,554 FTEs globally.

Product and Platform

We continue to lean into our ubiquity strategy, launching increased podcast support on connected Google and Alexa devices during the quarter. All Spotify users can now play and control podcasts through their Google Assistant-enabled device in English globally. Spotify is also now integrated into the PlayStation 5 and Xbox Series X|S gaming consoles, with the former featuring a dedicated Spotify button on the new media controller.

With all of the new content available on Spotify, we are continually making enhancements to the Home Tab to improve discovery and activation of content. In Q4, we launched our first-ever mixed-media morning show, The Get Up, in the US, where listeners get the best of both worlds with music and news. Additionally, Spotify users everywhere can now upload custom covers and descriptions to their homemade playlists using their mobile phones.

Content

We continue to lean into our goal of becoming the world’s number one audio platform through compelling new music and exclusive non-music content. As of Q4, we had 2.2 million podcasts on the platform (up from more than 1.9 million podcasts in Q3). Of note, 25% of our Total MAUs engaged with podcast content in Q4 (up from 22% of MAUs in Q3 2020). We continue to see strong growth in podcast consumption, with consumption hours in Q4 nearly doubling since Q4 2019. We have increasing conviction in the causal relationship between the growth in podcast consumption driving higher LTV and retention among our user base.

In an effort to grow audio monetization across the industry, we acquired Megaphone on December 8. Megaphone is one of the world’s most innovative platforms for enterprise podcast hosting and monetization. With this acquisition, we have the ability over time to make SAI technology available to third-party publishers on Spotify while growing our pool of targetable podcast inventory for advertisers.

In December, The Joe Rogan Experience became exclusive to Spotify, driving a meaningful uptick in audience for the show on our platform. As of year-end, The Joe Rogan Experience was the #1 podcast on our platform in 17 markets. While it remains early days, we are very encouraged by the performance of this content since its arrival on our platform, as it has stimulated new user additions, activated first time podcast listeners, and driven favorable engagement trends, including vodcast consumption. We also announced a new multiyear partnership with The Duke and Duchess of Sussex’s Archewell Audio. We were pleased with the performance of The Duke and Duchess of Sussex’s holiday special episode that was released on our platform in December 2020 and look forward to a full scale launch of shows coming in 2021.

Other notable Q4 content launches in the US included Dare to Lead with Brene Brown (Parcast), 10 Songs that Made Me (Spotify Studios), The Ringer Music Show (The Ringer), and The Get Up Morning Show (Gimlet). Internationally, we released 57 new Original & Exclusive (“O&E”) podcasts. Select launches included Caso 63, our first Original in Chile and ranked as one of the biggest fiction shows ever launched on the platform, as well as our first podcast in Telugu, Lifetime NTR (India), and 123 Segundos in partnership with BandNews (Brazil). We also signed 6 podcasts exclusively to our creator support program in Indonesia.

On the music front, key Q4 releases included Bad Bunny’s album, El Último Tour Del Mundo, Paul McCartney’s album, McCartney III,and more from the likes of Dolly Parton to Ariana Grande. Bad Bunny’s album was the first Spanish-language release to top the Billboard 200 chart in its 64-year history and, thanks to far-reaching international support across 24 markets, Spotify helped drive the Puerto Rican artist to historic heights. With the drop of Paul McCartney’s album, fans were given the opportunity to purchase a limited edition color vinyl, exclusive to Spotify users.

Two-Sided Marketplace

Our Sponsored Recommendations have continued a strong pace of growth, with December marking the single biggest month ever. During the quarter, we saw more than a 50% increase in the number of campaigns vs. the prior quarter. Additionally, over half of the customers in Q4 were new buyers, which helped drive an 82% increase in billings from the prior quarter. Notable campaigns included number one albums, El Último Tour Del Mundo by Bad Bunny and evermoreby Taylor Swift, as well as Welcome to O’Block by King Von and Pegasusby Trippie Redd.

We continue to add new features for the creator community and have seen a large increase in the number of artists and their teams using Spotify for Artists. This quarter, we expanded access to our popular feature, Canvas, which had been in limited beta. With Canvas, artists can upload short looping visuals to each of their tracks through Spotify for Artists, and in the first month since expanding access, over 180,000 artists used this tool. Canvas gives artists a powerful new way to develop fans on Spotify, and we have found that when listeners see a Canvas they are more likely to keep streaming (+5% on average vs. control group) or even share and save the track.

During December, we launched our annual Wrapped for Artists campaign, empowering artists around the world to reflect on and celebrate their year of growth on Spotify. Our 2020 Wrapped for Artists reached new heights, with over a 60% increase in peak engagement vs. 2019. We had our largest Wrapped for Artists of all time, with artists from over 200 countries around the world and more than 3 million visits to our microsite.

As part of our ongoing investments to elevate and support the songwriting community, in December, we rolled out the Songwriters Hub in Spotify — the new destination for fans and collaborators to explore their next favorite songwriter or producer. In the hub, visitors can find Written By playlists from both established and emerging songwriters, listen to podcasts about the craft of songwriting, and discover a rotating cast of featured songwriters and cultural moments each month. In our continued effort to connect fans to listeners, we debuted Weekly Music Charts for songs and albums in 46 new markets.

Free Cash Flow

Free Cash Flow was €74 million in Q4, a €95 million decrease Y/Y as the prior year included a favorable working capital benefit due to a shift in timing for select licensor payments while Q4 2020 included higher podcast-related payments. These decreases were partially offset by a decrease in net loss adjusted for non-cash items.

In addition to the positive Free Cash Flow dynamics, we maintain a strong liquidity position and are confident in the financial position of the business. At the end of Q4, we had €1.8 billion in cash and cash equivalents, restricted cash, and short term investments and no indebtedness1.

2021 OUTLOOK

In 2020, we believe the pandemic had little impact on our subscriber growth and may have actually contributed positively to pulling forward new signups. From a revenue standpoint, advertising was negatively affected in the back half of Q1 and persisted throughout the rest of the year. Looking ahead, we are optimistic about the underlying trends in the business into 2021 and beyond, however, we face increased forecasting uncertainty versus prior years due to the unknown duration of the pandemic and its ongoing effect on user, subscriber, and revenue growth.

The following forward-looking statements reflect Spotify’s expectations as of February 3, 2021 and are subject to substantial uncertainty. The estimates below utilize the same methodology we’ve used in prior quarters with respect to our guidance and the potential range of outcomes. Given the extraordinary operating circumstances we currently face with respect to the impact of COVID-19 there is a greater likelihood of variances within those ranges than typical quarters.

Q1 2021 Guidance:

Total MAUs: 354-364 million

Total Premium Subscribers: 155-158 million

Total Revenue: €1.99-€2.19 billion

Assumes approximately 770 bps headwind to growth Y/Y due to movements in foreign exchange rates

Gross Margin: 23.5-25.5%

Operating Profit/Loss: €(78)-€(28) million

Full Year 2021 Guidance:

Total MAUs: 407-427 million

Total Premium Subscribers: 172-184 million

Total Revenue: €9.01-€9.41 billion

Assumes approximately 370 bps headwind to growth Y/Y due to movements in foreign exchange rates

Gross Margin: 23.7-25.7%

Operating Profit/Loss: €(300)-€(200) million

#19

Spotify

Nuevo

Hola soy Alvaro un placer. Quería preguntar opiniones por si dejar hoy compra fuerte en AMD y alphabet o comprar fuerte en Spotify en espera de resultados de hoy?? Gracias buen día

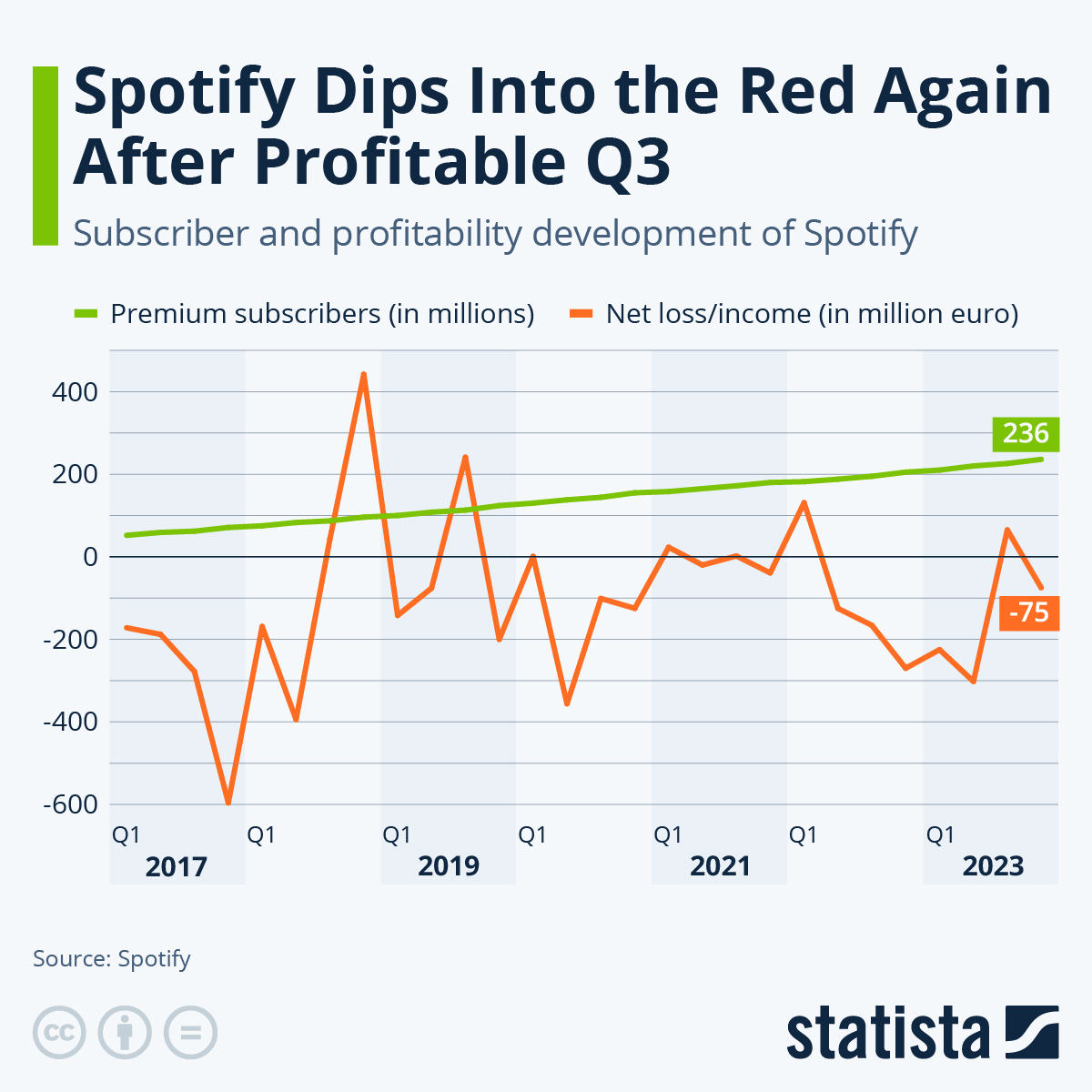

La compañía de producción y distribución de música y pódcasts en streaming Spotify registró unas pérdidas netas atribuidas de 34 millones de euros en el conjunto de 2021, lo que supone un descenso del 94% en comparación con los 'números rojos' que contabilizó durante el año anterior, según informó la empresa.

Los ingresos crecieron un 22,7% en el conjunto del año, hasta alcanzar los 9.668 millones de euros. Al tiempo, los costes asociados a los ingresos, derivados en gran medida de los derechos de autor que Spotify tiene que pagar a artistas y discográficas, se elevaron un 20,7%, hasta 7.077 millones.

Del total de la facturación anual, 8.460 millones de euros se correspondieron con las cantidades abonadas por los usuarios con suscripciones 'premium', un 18,6% más, mientras que los otros 1.208 millones se correspondieron con los ingresos por la publicidad servida a los usuarios que usan gratuitamente la aplicación, un 62,1% más.

Spotify cerró 2021 con 406 millones usuarios mensuales activos en el cuarto trimestre, un 18% más que en el mismo periodo del año pasado. De esa cifra, 180 millones eran suscriptores 'premium', un 16% más, mientras que otros 236 millones eran usuarios gratuitos, un 19% más.

En el conjunto del año, los gastos de ventas y marketing de la compañía se incrementaron un 10,3% más, mientras que los generales y administrativos fueron de 450 millones, un 1,8% más. La partida de investigación y desarrollo (I+D) fue de 912 millones, un 9% más.

Con respecto a los datos únicamente referidos al cuarto trimestre, Spotify contabilizó pérdidas de 39 millones de euros, un 68,8% menos que en el mismo periodo del año pasado. Al tiempo, la facturación creció un 24%, hasta 2.689 millones

#21

Re: Seguimiento de Spotify (SPOT)

Ghjer

La partida de investigación y desarrollo (I+D) fue de 912 millones, un 9% más.

me encanta esta partida, ¿que estaran investigando?¿estaran desarrollando una nave espacial?¿o sera la cura contra el cancer? desde luego no sera algo para Spotify que no es mas que una lista de canciones y ya esta, para eso no hay que investigar nada.

La plataforma de producción y distribución de música y pódcast en 'streaming' Spotify cerró el primer trimestre de 2022 con un beneficio neto de 131 millones de euros, lo que supone multiplicar por 4,7 las ganancias observadas en el mismo periodo de 2021, según se desprende de la cuenta de resultados que ha publicado este miércoles la empresa.

Los ingresos crecieron un 23,9%, hasta alcanzar los 2.661 millones de euros, al tiempo que los costes asociados a los ingresos, derivados en gran medida de los derechos de autor que Spotify tiene que pagar a artistas y discográficas, se elevaron un 24,5%, hasta 1.990 millones de euros.

Del total de facturación, 2.379 millones procedieron de las suscripciones de usuarios 'premium', un 23% más, mientras que los otros 282 millones procedieron de la publicidad servida a los usuarios que usan gratuitamente el servicio, un 31% más.

El número total de usuarios entre enero y marzo fue de 422 millones, un 19% más. Los suscriptores 'premium' crecieron un 15%, hasta 182 millones, al tiempo que los usuarios gratuitos avanzaron un 21%, hasta 252 millones.

La empresa ha indicado que perdió 1,5 millones de suscriptores de pago como consecuencia de su decisión de dejar de operar en Rusia.

Los costes de ventas y marketing fueron de 296 millones de euros, un 25,4% más, mientras que los generales y administrativos se elevaron cerca de un 30%, hasta 131 millones. La partida de investigación y desarrollo (I+D) fue de 250 millones, un 27,6% más.

De esta forma, en los últimos 12 meses la empresa ha empeorado ligeramente sus márgenes. Si en el primer trimestre de 2021 el resultado operativo fue de 14 millones, en el primer trimestre de este año fue negativo en seis millones de euros. El abultado cambio en los beneficios se debe al impacto positivo de 175 millones por ingresos financieros

Visión de B&H sobre Spotify Spotify. Es el famoso servicio de música por streaming. Posiblemente una de las apuestas más visionarias de nuestra cartera de acciones. Es la única empresa de nuestra cartera que no genera beneficios hoy en día, aunque sí un flujo de caja positivo. Dicho esto, el servicio de streaming de Spotify es excelente y es el líder en el mundo de la música compitiendo contra grandes gigantes como YouTube o Apple Music. El servicio es absolutamente magistral para sus usuarios. Además, recientemente ha entrado en el negocio de los podcasts y audiolibros donde el crecimiento potencial es enorme, especialmente teniendo en cuenta el buen desempeño realizado hasta ahora en el negocio de música. Esta es la razón por la que la empresa no ha generado aún beneficios: porque no para de invertir en estas nuevas áreas de negocio, aunque evidentemente está sentando las bases para un gran crecimiento futuro de ventas y beneficios. Daniel Ek, fundador y CEO, es muy optimista y ambicioso con las posibilidades de Spotify. El pasado 8 de junio tuvo su Día del Inversor, en el que indicó que esperaba beneficios operativos de alrededor de USD 20.000 millones a largo plazo (diez años), que es la capitalización actual de la empresa. El precio de la acción ha caído al nivel más bajo desde su salida a bolsa en 2018 a pesar de que en estos tres años (2018-2021), Spotify ha generado un flujo de caja positivo cada año y ha multiplicado por dos el número de sus abonados y la facturación. Tanto Ek como Martin Lorentzon, cofundador, son miembros del Consejo y cuentan con una participación conjunta del 18% en el capital de la empresa.

Las acciones de Spotify caían un 14,7% en Bolsa de Nueva York este martes, hasta los 139,7 dólares (126,44 euros), después de que la compañía haya anunciado pérdidas en el segundo trimestre del año y su decisión de aumentar los precios de su plan 'premium' en una docena de país, entre ellos España.

En concreto, la empresa de servicios multimedia subirá un euro el precio de sus planes 'premium' en varios países, entre los que se encuentra España, de manera que el nuevo plan individual 'premium' costará 10,99 euros, el dúo 'premium' 14,99 euros y el familiar premium 16,99 euros, según afirma la agencia alemana DPA.

"El panorama del mercado ha seguido evolucionando desde nuestro lanzamiento. Para que podamos seguir innovando, estamos cambiando nuestros precios Premium en una serie de mercados de todo el mundo", ha destacado la compañía.

Por otro lado, este martes se presentaron los resultados de la compañía, donde se registraron pérdidas operativas por valor de 247 millones de euros, un 27,3% más altas que las registradas en el mismo período del año anterior.

Las pérdidas operativas ajustadas de 112 millones de euros superaron las previsiones, excluidos los gastos relacionados con las medidas adoptadas en el trimestre para racionalizar las operaciones y reducir costes.

Tras este anuncio, Spotify registraba a las 18.45 horas (hora española) una caída en sus títulos en la Bolsa de Nueva York de hasta un 14% en comparación al cierre del día anterior, que se situó en los 163,72 dólares (148,18 euros), aunque la compañía presenta una revalorización del 77% en el acumulado del año

#30

Re: Seguimiento de Spotify (SPOT)

Nuevo

Hola soy, placer. Quería preguntar opiniones por si dejar hoy compra fuerte en AMD y alphabet o comprar fuerte en Spotify en espera de resultados de hoy?? Gracias buen día